What Is a Medicare Supplement Plan?

Find out about Medicare Supplement Plans, how they work, the eligibility requirements, and how much a policy could cost you.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

Receiving a medical bill that’s higher than what you expected can be overwhelming.

Since Medicare doesn’t cover all of these expenses, millions of Americans get Medicare Supplement Insurance Plans to help them cover the rest of the costs.

Before joining one of these policies, it’s important to fully understand what the insurance covers and if it will benefit you long term.

This article will break down what Medicare Supplement Plans are, how they work, the eligibility requirements, and how much the policies could cost you.

A Closer Look at Medicare

Medicare is a government-run health insurance for people 65 or older, certain people under 65 with disabilities and people of any age with End-Stage Renal Disease (ESRD).

There are different parts of Medicare that help cover different services. Part A covers the care and treatment of patients in hospitals or other medical facilities. For example:

Part B covers outpatient care and services. This includes bills for physical therapy, specialist consultations, and rehabilitation.

Part B also helps cover preventative services like vaccines and screenings, as well as the cost of wheelchairs and walkers.

The Medicare Part D plan helps with prescription drug coverage. These plans are run by private insurance companies.

Supplement Plans Explained

A Medicare Supplement Plan (also known as Medigap) is a health insurance policy that you can buy from private companies.

These plans help you pay for the remaining out-of-pocket costs that Medicare Part A and B don’t cover.

Some of the common medical costs that Medicare doesn’t cover are:

In most states (except Wisconsin, Massachusetts, or Minnesota) there are 10 standard Medicare Supplement Plans available for you to choose from. We’ll go into more detail about this later in the article.

Depending on which plan you choose, the Supplement Plan could pay for:

Part of the expense that Medicare doesn’t cover (this is called the deductible)

20% of the amount you’re responsible for paying (the co-payment)

Any other health care costs

Terms you need to know:

Deductibles: This refers to the amount you must pay for covered health care services before your insurance begins to pay.

Co-payment: An amount you might have to pay as part of your share of the cost for a visit to the doctor or for a prescription drug. Co-payments are usually a set amount rather than a percentage. For example, you might have a co-payment of $25 for a doctor's visit.

A licensed insurance company also can’t sell you a Medicare Supplement Plan if you already have Medicaid or a Medicare Advantage Plan.

Medicaid is a government-run program that helps people with limited resources and income with medical expenses.

Also known as Medicare Part C, a Medicare Advantage Plan is hospital and medical insurance provided by private insurance companies instead of the federal government.

One of the other benefits of Medicare Supplement Insurance is that they are “guaranteed renewable.”

This means that as long as you continue paying the premium, your Medicare Supplement Plan will be renewed each year and your coverage will continue—even if you develop health problems.

New to Medicare? Here Are Some Key Takeaways:

Medicare Supplement Plans have been designed to pay for the expenses that Medicare Part A and B don’t cover.

To be eligible for a Medicare Supplement Insurance, you must first be enrolled in Parts A and B.

You cannot buy a Medicare Supplement Plan if you already have Medicaid or a Medicare Advantage Plan.

Medicaid is a federal and state program that helps people with limited resources and income with medical expenses. A Medicare Advantage Plan (also known as Medicare Part C) is medical and hospital insurance provided by private insurance companies, instead of the federal government.

Medicare Supplement Plans are also “guaranteed renewable.” As long as you continue paying the premium, your plan will be renewed each year and your coverage will continue—even if you develop health issues.

How Do I Enroll in a Medicare Supplement Plan?

If you want to enroll in a Medicare Supplement Plan, you must first have Medicare Parts A and Parts B.

The best time to enroll in one of these plans is during the Medicare Supplement Open Enrollment Period.

Not only are you likely to get better prices and have more choices available to you, but you also won’t have to answer any health questions.

If you enroll outside of this window, you will be at risk of having to pay higher premiums and have fewer coverage options.

This window only happens once in your life (unless you collect Social Security Disability Income) and lasts for six months.

This six-month window will start on the first day of the month that your Medicare Part B enrollment is effective. You must also be 65 or older for the Open Enrollment Period to begin.

The Medicare Supplement Open Enrollment Period must not be confused with the Fall Annual Enrollment Period, which takes place every year between 15 October and 7 December.

During these months you can enroll, disenroll or change Medicare Advantage and Part D prescription drug plans.

What Should I Expect to Pay?

Before buying a Medicare Supplement Plan, it’s important that you are aware of how much it could cost you long term.

Although the plans are generally standardized across America, the prices will vary depending on which state you live in.

However, Wisconsin, Minnesota, and Massachusetts all have their own versions of Medicare Supplement Insurance Plans.

There are three ways insurance companies set premiums. These include:

Community-rated: This premium is not based on your age. This means that the same monthly premium is charged to everyone. However, the price will vary according to inflation.

Issue-age rated: This premium will be based on the age you are when you buy the policy. Therefore, the premium is lower for people who buy it at a younger age and won’t change as they get older.

Attained-age rated: This premium is based on your current age and will go up as you get older. Although these premiums might be the least expensive at first, they will eventually become the most expensive and are also affected by inflation.

Before buying a Medicare Supplement Plan, remember to compare them carefully and find the one that works best for your needs and budget.

This is because the cost of Medicare Supplement Plans can vary significantly. Different insurance companies may charge different premiums for exactly the same basic benefits.

If you’re considering buying a Medicare Supplement Plan from one insurance company, be sure to compare the price of the plan with another.

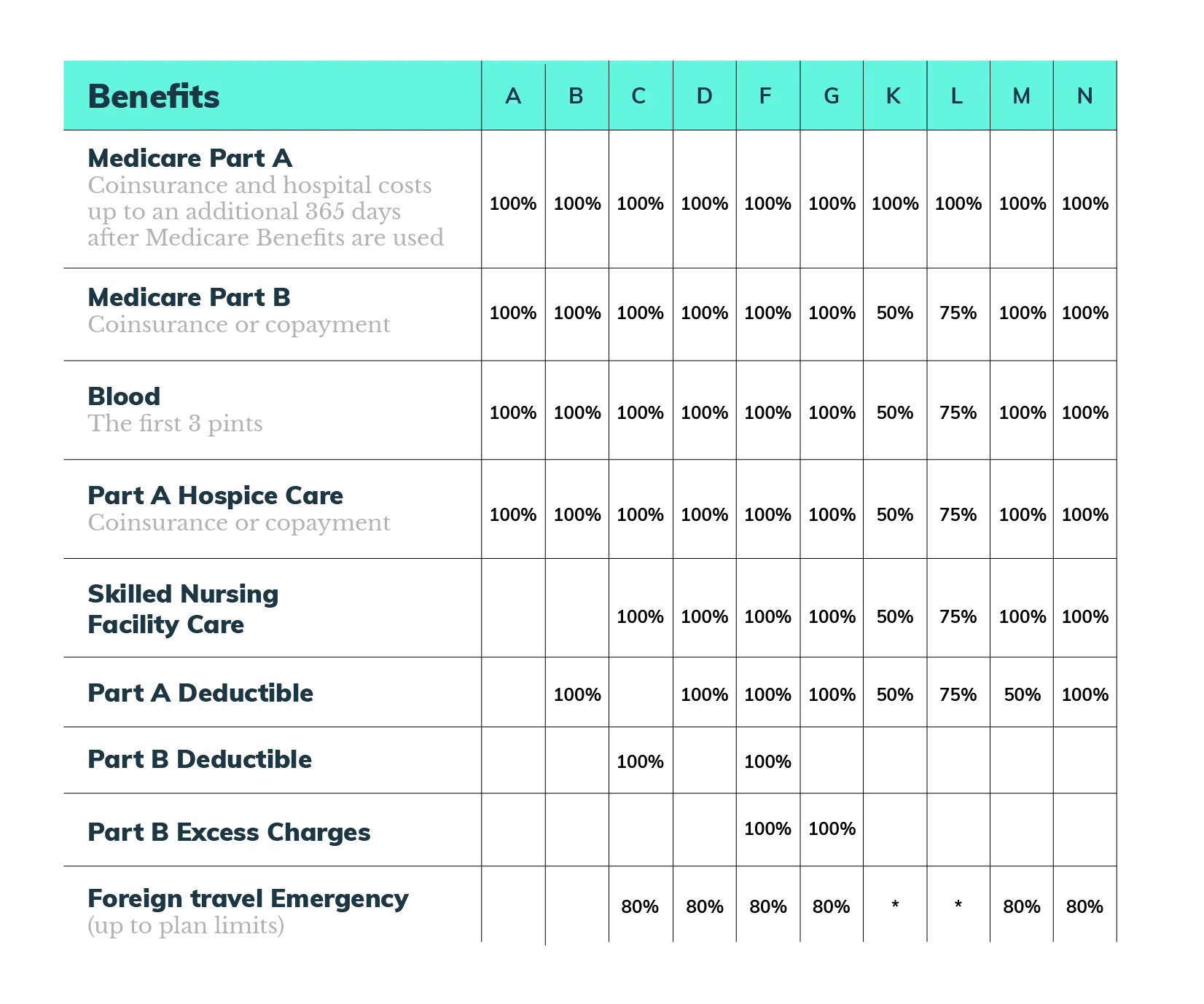

What Are the 10 Different Medicare Supplement Plans?

Now that you have a better idea of what Medicare Supplement Plans are, let’s take a closer look at each plan.

The table below summarises the different benefits that each plan covers.

Where a percentage appears, the Medicare Supplement Plan covers the percentage of that benefit and you must pay the rest.

*Out-of-Pocket Limit

However, some of these plans have a bit more to them. For example:

Plans F and G: In some states, these plans offer a high-deductible plan. If you decide to choose one of these plans, you must pay a deductible fee of $2,370 before your insurance pays anything.

Plans K and L: These plans have out-of-pocket limits of $6,220 and $3,110. Once you have paid these amounts and the Part B deductible ($233), the plan will pay 100% of your covered services for the rest of the year.

Plans C and F will not be available to people who are newly eligible for Medicare Supplement Plans on or after 1 January 2020.

Plan N will pay 100% of the Part B coinsurance. However, you will have to pay up to $20 for doctor visits and $50 to go to the emergency room (as long as you are not admitted to the hospital).

The table above shows that it’s very important that you read the fine print and understand what each Medicare Supplement Plan covers.

Apart from the monthly premium, you also need to think about the out-of-pocket expenses and what you can reasonably afford when the premiums go up each year due to inflation.

Can I Get a Medicare Supplement Insurance Plan If I’m under 65?

Some people have Medicare before turning 65 because they have a disability or ESRD.

Although federal law doesn’t require insurers to sell Medicare Supplement Plans to people under 65, some states do require insurance companies to sell at least one Supplement Plan to people under 65. These include:

If you are still unsure, contact your State Insurance Department to see what your Medicare rights are under state law.

This is the process an insurance company uses to decide (based on your medical history) whether to provide you with healthcare insurance, add a waiting period for pre-existing conditions, and how much to charge you for the Supplement Plan.

The waiting period refers to a delay in Medicare basic benefits due to pre-existing conditions. This means that you might have to cover the medical expenses for up to six months after the Medicare Supplement Plan begins.

You can avoid or shorten this pre-existing condition waiting period if you buy a Supplement Plan during the Open Enrollment Period.

Find a Medicare Supplement Plan That’s Right for You

At PolicyScout, we know that choosing a Medicare Supplement Plan gets confusing very quickly.

Luckily, we’ve reviewed and ranked the top providers to help you find the right plan for your needs and budget.

Talk to one of our licensed Medicare insurance experts risk-free and at no charge.

Medicare Supplement Plans FAQs

What Is Medicare?

Medicare is government-run health insurance for people 65 or older, certain people under 65 with disabilities, and people of any age with End-Stage Renal Disease (ERD).

Is Medicare the Same as Medicaid?

No, Medicare is not the same as Medicaid. Medicare is health insurance for people 65 or older, certain people under 65 with disabilities, and people of any age with End-Stage Renal Disease (ERD). Medicaid is a federal and state program that helps people with limited resources and income with medical expenses.

What Is a Medicare Supplement Plan?

A Medicare Supplement Plan is a health insurance policy that is designed to help people pay for some or all of the costs not covered by Medicare Parts A and B.

Am I Eligible for Medicare Supplement Insurance?

If you are covered by Medicare Parts A and B, you qualify for Medicare Supplement Insurance.

When Can I Enroll in a Medicare Supplement Plan?

The best time to enroll in a Medicare Supplement Plan is during the Open Enrollment Period. This is a six-month window that will start on the first day of the month that your Medicare Part B enrollment is effective.

Will a Medicare Supplement Plan Cover the Cost of Prescription Drugs?

Medicare Supplement Plans are designed to cover what Part A (hospital and other registered medical facilities) and Part B (outpatient facilities) won't pay for. To get coverage for prescription drugs, you will need a Medicare Part D plan or Medicare Advantage.

Does Everyone Need Medicare Supplement Insurance?

No. If you already have other types of health coverage the “gaps” in your Medicare expenses may already be covered. You won’t need a Supplement Plan if:

You belong to the Medicare Advantage plan.

Medicaid or the Qualified Medicare Beneficiary (QMB) Program covers your Medicare premium and other additional expenses.

An employer group health plan covers your medical expenses.

What Happens If I Don’t Pay My Medicare Premiums?

If you stop paying your Medicare premiums you will be at risk of losing your medical coverage. However, this will not happen without warning.

How Can I Find Out More about My Medicare Options?

Visit the official Medicare.gov website, speak to the Social Security Agency, or reach out to PolicyScout to learn more about your Medicare and Medicare Supplement Plan options.