What Is Medicare Part C?

Find out about costs, benefits, and enrollment with our 2022 guide to Medicare Advantage and see if it's right for you.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

You’ve probably looked at the different Medicare plans, seen Parts A, B, and D, and wondered, “What happened to Part C?”.

These days what was called Part C is now called Medicare Advantage. Like Part C plans in the past, Medicare Advantage is an umbrella term for health cover plans offered by private Medicare insurers.

Read on to learn about coverage, costs, and benefits of Medicare Part C (Medicare Advantage).

Medicare and Health Insurance in the U.S.

With the rising cost of quality health care in the U.S. in recent decades, it has become crucial for older Americans to learn about different plans and options.

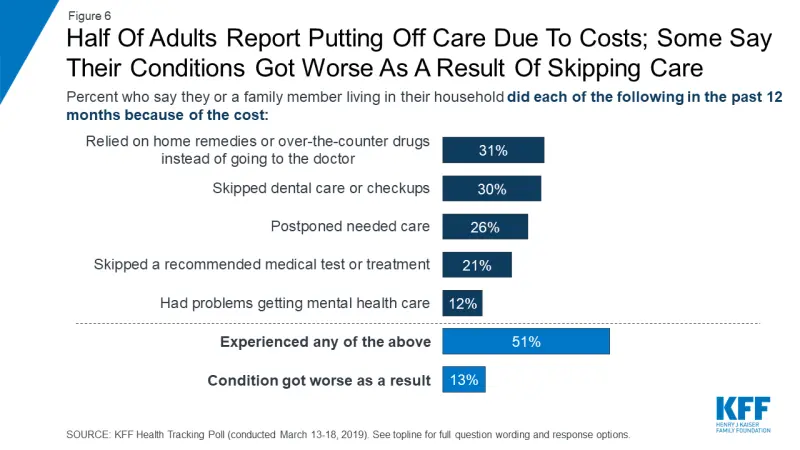

In 2019, just over half of the adult population put off their medical care because of costs. (Source: KFF)

Medicare is one such option that millions of Americans use to ensure their health and wellbeing as they age.

Medicare gives people over the age of 65, disabled individuals, and those suffering from terminal illnesses like ESRD (End-stage Renal Disease) affordable health care options.

A Recap of the Different Parts of Medicare

Medicare Part A refers to all inpatient or hospital medical expenses.

Medicare Part B covers outpatient medical expenses such as consultations.

Medicare Part D relates to self-administered prescription medication.

Original Medicare vs Medicare Advantage (Part C)

You can apply for Medicare cover through two different plans—Original Medicare and Medicare Advantage.

Both types of plans follow the same enrollment rules, and you must sign up before your 65th birthday to avoid penalties.

Original Medicare

Medicare is a federal government health insurance program that covers inpatient (Part A) and outpatient (Part B) medical expenses.

With Original Medicare, you can sign up for either Medicare Part A and Part B or both. You'll also have the option of enrolling in a standalone Part D plan at an additional monthly cost.

If you choose to enroll with Original Medicare, you may pay a monthly premium for Part A coverage. You will also have to pay an additional monthly fee to get Part B cover.

For example, if you turn 65 next month you can sign up for Original Medicare through the Social Security Agency website.

You'll have to decide if you want Part B coverage, and you will have to find a Part D insurance provider to get coverage for prescription drugs.

Medicare Advantage

Medicare Advantage plans are offered by private health insurance companies which have been contracted into the federal Medicare program.

When you sign up for a Medicare Advantage policy, you'll have to pay a monthly amount just like you would with Medicare Part A and B coverage.

What makes Medicare Advantage different from Original Medicare is that Part A, Part B, and Part D coverage costs are paid together. Medicare Advantage members also receive additional cover for certain medical expenses.

For example, if you signed up for Medicare and joined a Medicare Advantage plan, you would pay Medicare Part A and B premiums in one monthly payment and get additional prescription drug coverage.

People usually change to Medicare Advantage because it offers a cost-effective and straightforward way to manage Medicare expenses.

The range of providers across the U.S. means that people can compare different plans and find a policy suited to their needs.

Generally, Medicare Advantage offers more benefits and options than Original Medicare, such as flex cards, access to fitness programs, and dental and vision coverage.

With an Advantage plan, there is always the option of changing providers if you become unhappy with their service.

Differences in coverage between Original Medicare and Medicare Advantage| Original Medicare | Medicare Advantage | |

|---|---|---|

| Part A Coverage | ✓ | ✓ |

| Part B Coverage | ✓ | ✓ |

| Part D Coverage | X | ✓ |

| Additional Medical Benefits | X | ✓ |

The Different Medicare Advantage Options

Understanding your options around Medicare cover can be tricky. Most people don’t know that there are different kinds of Medicare Advantage policies available to them.

If you're thinking of joining a Medicare Advantage plan, you should weigh up the pros and cons of each type of coverage and think about your circumstances before deciding on a health care plan.

Whether you choose an HMO, PPO, PFFS, or MSM, it's essential to know how these schemes operate and what coverage they offer their members.

We've provided an overview of the most popular options and given you a breakdown of the benefits of each plan.

Health Maintenance Organization (HMO)

HMOs, or Health Maintenance Organizations, are among the more popular health coverage plans in the U.S.

They work by offering clients access to local physicians, hospitals, and medical providers in their network.

If you sign up for an HMO, you’ll likely have to choose a network physician who will become your primary care doctor.

You'll also only be able to use doctors and medical specialists who are network providers.

HMO structures allow Medicare Advantage providers to charge their clients lower premiums and reduced rates for medical expenses.

Another benefit of HMOs is that health care plans can ensure the quality of treatment and protect customers from sub-par medical care.

A drawback is that people are limited with the doctors and medical facilities they can use.

It’s likely that if you go outside of your network, your HMO won’t pay for services or costs.

Preferred Provider Organization (PPO)

PPOs, or Preferred Provider Organizations, are another common type of health coverage plan that offers similar benefits to HMOs.

If you sign up for a PPO, you'll be able to visit a more extensive network of health care professionals. Still, it will generally cost you more to join a PPO than an HMO.

Some people prefer PPOs because they get to see medical specialists who aren’t available through an HMO.

Another difference is that your PPO will still cover some of the costs of medical services if you decide not to use their preferred provider network. However, you should expect to pay more if you choose to do so.

If you go to a doctor on your PPO's network you might pay $120.00 for the consultation, but you could pay $160.00 for service if you use an out-of-network doctor.

Private Fee-for-Service (PFFS)

A PFFS plan is an alternative to Medicare Advantage HMOs and PPOs, where you pay a predetermined price for treatment and medical services.

PFFS coverage offers people more flexibility in seeking out medical care than HMOs and PPOs.

There are usually no limits to who you can see (as long as your physician agrees to treat you under the terms of your PFFS plan).

For example, if you were to visit the doctor and the bill came to $160.00, as a member of a PFFS plan you would pay a set amount (let's say $25.00) and your PFFS provider would cover the remaining balance.

Special Needs Plan (SNP)

SNPs are Medicare Advantage plans designed for special needs individuals within the Medicare system.

These plans usually have strict criteria for membership and are required to focus on specific groups of people. These are:

1) People who live in certain institutions (like a nursing home or mental health facility).

2) People who are eligible for Medicare and Medicaid (known as dual eligibles).

3) People who suffer from a specific chronic or disabling condition, such as dementia or chronic heart failure.

SNPs provide services and coverage for expenses related to their area of focus and have networks of specialist doctors and health care providers.

By law, all SNPs must provide prescription drug coverage (Part D) to their members. Usually, members will have to choose a primary doctor for medical checkups, consultations, and health care services.

How Do I Enroll for Medicare Part C (Medicare Advantage)?

The first step in enrolling for a Medicare Advantage plan is determining whether you are eligible to do so.

You can enroll in a Medicare Advantage policy if:

You are 65 years old (or turning 65), have a disability, or suffer from a disease such as End-Stage Renal Disease (ESRD).

You are a U.S. citizen or lawfully present in the United States and enrolled in Original Medicare Part A or Part B.

You are not part of a Medigap, Medicare Supplement Plan, Prescription Drug Plan (Part D), or on Medicaid.

You are living in the service area of the plan you want to join. This means that you can't join a Part C plan in a state or county where you don't reside. For example, if you live in Pennsylvania you can’t join a plan that services California or Alaska.

The next step is to find an insurance company that offers a Medicare plan to suit your medical needs and financial circumstances.

Finding a plan can be challenging. People are often confused by the complicated terms (deductibles, coinsurance, out-of-pocket costs, thresholds) and different plan structures (HMOs, PPOs, PFFS) offered.

Once you're satisfied with the provider's type of plan and the costs of enrolling, you should visit their website or contact them to sign up as a member during the correct enrollment period.

Companies will allow you to sign up online, over the phone, or in person. However, it is essential to remember that you should never give out your Social Security number or Medicare card number over the phone.

Depending on your Medicare enrollment status, registration can take anywhere from one week to a couple of months. You should regularly contact your Medicare insurance provider to determine how far along they are with your application.

Once you're enrolled, your plan will tell you when your coverage starts and what you must pay each month.

Need further assistance with signing up for a Medicare Advantage plan? PolicyScout can provide you with information and guidance on how you can do this.

Our experienced consultants can also offer guidance on the best Medicare Advantage policies in your area if you’re struggling to decide which plan is right for you.

Important Enrollment Dates for Medicare Advantage

Applying for and changing your Medicare coverage at the right time of the year can save you time and money. Remember these important enrollment dates to get on top of your Medicare.

Initial Enrollment Period (7-month window): If you are new to Medicare, you can enroll three months before and after the month of your 65th birthday.

Open Enrollment Period (October 15, 2021 – December 7, 2022): During this period, you can join, switch or end a Medicare Part C plan without penalties.

Medicare Advantage Open Enrollment Period (January 1, 2022 – March 31, 2022): During this period, you can switch Medicare Advantage plans or move from a Medicare Advantage plan to Original Medicare.

5-Star Special Enrollment Period (December 8, 2021 - November 30, 2022): If you decide to change your current Medicare Advantage plan to a five-star rated Medicare Advantage plan, you can do this without having to pay a penalty.

What Does It Cost to Enroll in a Medicare Advantage Plan?

The costs of enrolling in a Medicare Part C plan will vary depending on your state, the health care provider, and your level of cover.

When you join a Medicare Advantage plan, you will still be liable for your monthly Medicare premiums.

Here are a few examples of what costs you might expect to pay when joining a Medicare Advantage plan.

1) If you're up to date with your Medicare tax contributions, this will mean that you pay:

- Nothing to enroll in Medicare Part A.

- A monthly premium (based on your income) to access Medicare Part B cover.

- A monthly Medicare Part C premium.

2) If you aren't up to date with your Medicare tax contributions, you'll pay:

- A monthly premium to enroll in and use Medicare Part A.

- A monthly amount based on your income to access Medicare Part B cover.

- A monthly Medicare Part C premium.

3) If you are over the age of 65 but haven't enrolled in any form of Medicare and haven't contributed through Medicare taxes, you'll pay:

- A penalty to join Medicare Part A.

- A monthly premium to enroll in and use Medicare Part A.

- A penalty to join Medicare Part B.

- A monthly amount (based on your income) to access Medicare Part B cover.

As seen above, if you join a Medicare Advantage plan you won’t have to pay excess fees or more than you would if you had Original Medicare. Many of the penalties and monthly premiums are the same for both types of plans.

If you’d like to learn more about the cost of enrolling in Original Medicare or Medicare Part C plans, send an email to Help@PolicyScout.com to get in touch with one of PolicyScout’s experienced health care consultants.

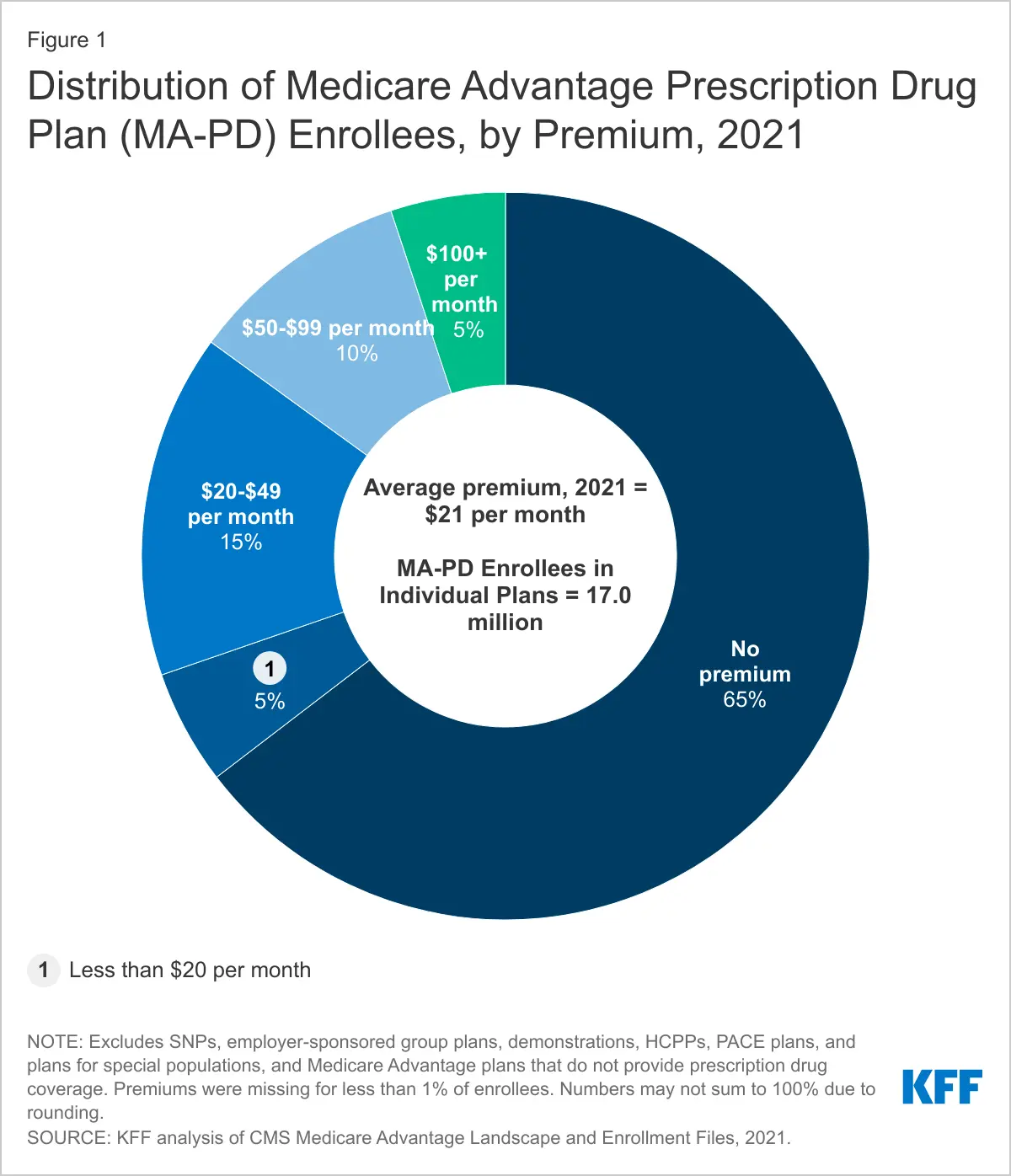

A Breakdown of the Different Premiums Paid for Medicare Advantage Plans in 2021

As seen in this diagram provided by the Kaiser Family Foundation, around 65% of Medicare Advantage members did not pay monthly premiums, while 35% did. Finding the right Medicare Advantage provider is key to lowering your health care insurance costs.

What Procedures and Costs Will Medicare Advantage Cover?

Because Medicare Advantage plans cover all Part A and Part B expenses and even Part D costs, you'll be covered for most medical expenses and procedures.

Medicare Advantage works similarly to Original Medicare, and your plan will usually pay the total or part of the cost for Part A and Part B expenses.

This means that you’ll get the same or even more health care coverage for doctor visits, hospital stays, and unforeseen medical expenses.

The majority of Medicare Advantage plans also offer prescription drug coverage (Part D). 90% of Medicare Advantage enrollees have some form of Part D insurance in 2021.

Along with this, many Medicare Advantage plans offer supplemental benefits. These benefits cover medical services such as eye exams, hearing exams, meal benefits, and dental care. Some plans will offer flex cards, that allow members to purchase medical equipment and other necessary items.

Additional health supplements are a large drawing card for many people to join.

Usually, these costs (eye exams, dental care, hearing aids, etc.) aren't covered by Original Medicare.

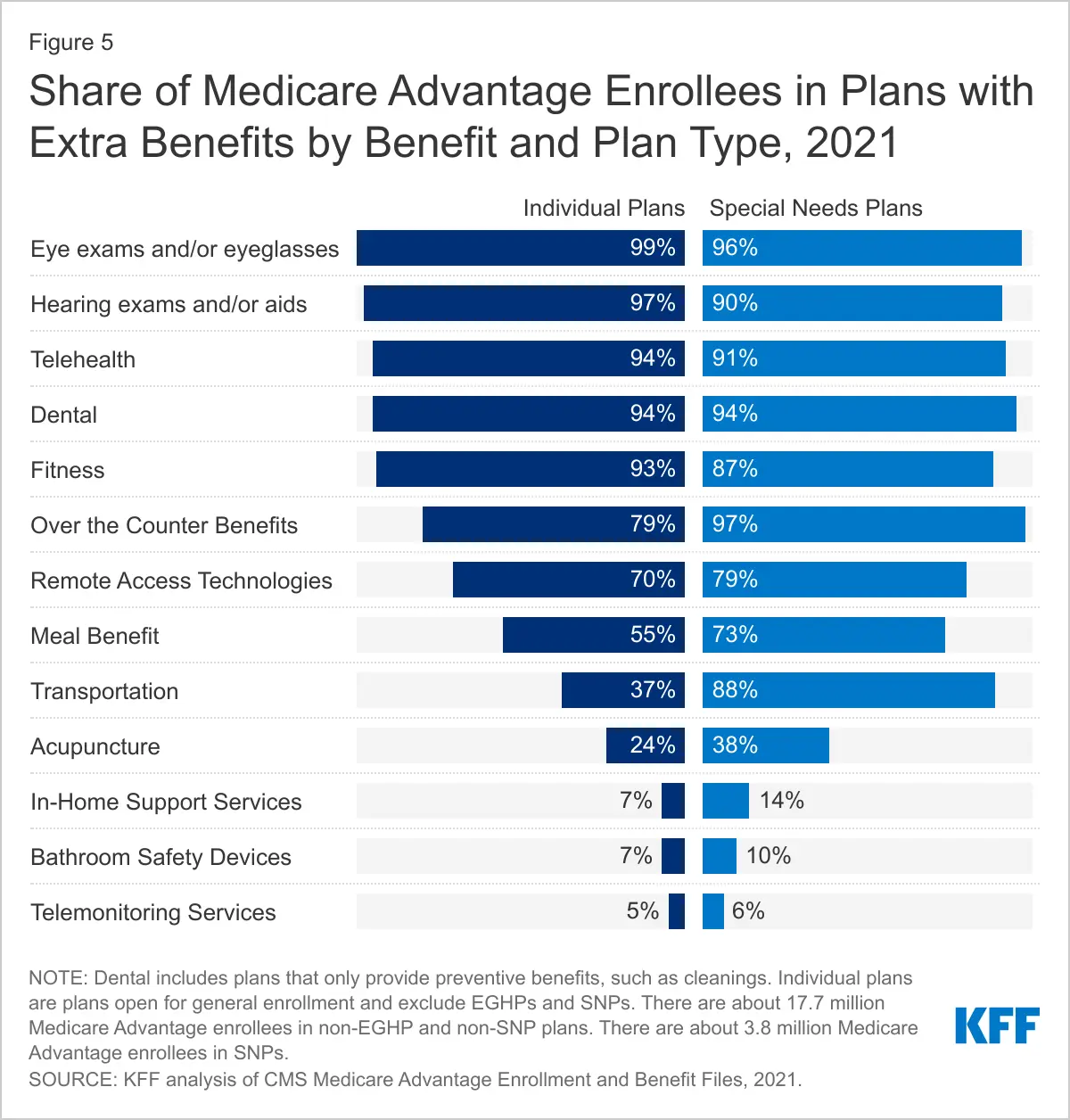

Some of the Supplemental Medical Benefits for Medicare Advantage members

This KFF diagram shows that Medicare Advantage plans offer a range of supplemental health benefits not available through Original Medicare. Nearly all Medicare Advantage plans cover eye exams and eyeglasses, and some even pay for acupuncture.

Your coverage will be different for each plan. Still, a key takeaway is that if you sign up for Medicare Advantage you'll get comprehensive coverage for most Part A, Part B, and Part D medical expenses.

However, the variety in the benefits and costs for various Medicare Advantage plans means you'll have to look through different policy options to find out what will be covered.

This can be confusing for many people, as many Medicare Advantage plans offer location-specific benefits and prices.

Need help navigating the hundreds of health care options available to you? PolicyScout can provide you with information and guidance to make the process stress-free and straightforward.

Our consultants will answer your questions and direct you to some of the best options based on your needs. Reach out to us by email or phone if you need assistance choosing a Medicare Advantage plan.

Different Plans Have Different Benefits

Because there's so much variety in the services and benefits offered by different Medicare Advantage Plans, shopping around for a Medicare insurance plan that suits you can get tricky.

Many Medicare Advantage plans don’t charge monthly premiums, and offer in-network benefits like no copayments for doctors visits and lab services.

Some Medicare Advantage plans offer members free access to network health providers and even cover the cost of prescription medicine.

Some Medicare Advantage plans even have fitness perks, travel cover, and other health care benefits you wouldn't usually receive through Medicare.

PolicyScout can help you make sense of your options and find the top health insurance providers in your area. Speak to a consultant to learn more about the different plans you can join.

Out-of-Pocket Costs and Medicare Advantage (Part C)

Each Medicare Advantage plan has a threshold for annual out-of-pocket expenses. This is required by law and is a cap or limit on how much you will have to spend before your Medicare Advantage plan covers your medical bills.

In 2021, the average out-of-pocket limit for Medicare Advantage Part A and B costs is $7,550.00 for in-network services and $11,300.00 for combined in-network and out-network services.

What does this mean? Your potential out-of-pocket medical expenses are limited to $7,550.00 (in-network) and $11,300.00 (out-network) per year. After this threshold is met, your Medicare Advantage plan is required to cover 100% of the costs.

Your out-of-pocket expenses will depend on your plan's terms, structure (HMO vs PPO), and coverage.

Because private insurance companies offer Medicare Advantage plans, there will be variety in your coverage, benefits, and costs.

It's best to determine what your plan will cover and how much you might pay before signing up.

Once you enroll with a Medicare Advantage plan, you’ll only be able to change or modify your coverage during certain times of the year (see Important Enrollment dates for Medicare Advantage).

Before you decide to enroll in a plan, learn more about the different programs on offer and how you can make the most of your Medicare Advantage cover. PolicyScout's team will help you find the right plan.

What Do I Do If I Haven’t Paid Medicare Taxes?

Joining a Medicare Advantage plan won't be affected by your Medicare tax contribution history.

But you will have to pay a penalty amount on top of your monthly fees if you haven't contributed to Medicare through payroll for at least ten years.

In some cases, your Medicare insurance company might offer to pay a part of your Medicare Part B premiums. Still, it's essential to check first before signing on to a plan.

If you want to learn more about Medicare Advantage providers in your area, reach out to an expert advisor from PolicyScout. We’ll be able to help you find the right plan for your health care coverage.

How Do I Find Out More about My Health Care Coverage?

Medicare Advantage plans offer benefits and services you wouldn't usually get with Original Medicare, such as dental and vision coverage, and cover for the costs of prescription drugs.

However, the number of providers and policy options makes it hard to decide which plan is right for you.

If you want to learn more about Medicare and Medicare coverage, we’d recommend you check out our Medicare Hub to learn about the different sections of health coverage available to you.

In it, we've got information on Medicare, Medicare supplement insurance, and Medicaid, as well as a range of other topics to help you get up to speed with health coverage and the Medicare program.

If you have any questions or would like to speak to a health care consultant, the PolicyScout team is ready to assist you.

You can contact us by phone at 1-888-912-2132 or email us at Help@PolicyScout.com to get your Medicare, Medicare Supplement Insurance, and Medicare Advantage questions answered.