What Is Medicare Part D?

Learn More about Your Health Care Options with PolicyScout’s Guide to Medicare Part D.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

Medicare is a federal government initiative that provides affordable healthcare options to senior citizens, disabled people, and people who suffer from chronic conditions such as ESRD (End-Stage Renal Disease).

Part of the Medicare program has to do with prescription medications that people use at home. This is known as Medicare Part D.

In this article, we’re going to cover Medicare Part D, the different prescription drug coverage options, how you can join a Medicare Part D plan, and the costs of enrolling.

(Source: Pexels)

Where Does Medicare Part D Fit In?

Medicare Part D insurance covers the costs of self-administered prescription drugs.

These include medications such as antibiotics, pain medication, blood pressure tablets, and cholesterol tablets prescribed to you by a medical doctor and administered by yourself.

The Other Parts of Medicare

Medicare Part A deals with hospital or inpatient medical expenses.

Medicare Part B covers outpatient expenses such as doctor’s visits, scans, blood tests, and other medical costs.

Medicare Part C (now called Medicare Advantage) are private insurance plans that offer Part A, B, and D cover plus additional health care benefits.

For example, let's say you were to be diagnosed with a heart condition and prescribed medication to lower your blood pressure. The cost would be covered partly or entirely by Medicare Part D if you have a Prescription Drug Plan.

Determining If Your Medicine Is Covered by Part D Insurance

Use these four questions to find out if you can claim your prescription medication as a Part D expense:

Are you currently an admitted hospital patient?

Is the medication you’re using prescribed by a registered doctor?

Do you control when and how you take your medication?

Is your medication approved by your Part D health care provider?

If you answered no to the first question and yes to the last three questions, your medication should be covered by your Part D health care plan.

Important Notes:

You should also check with your Medicare drug plan to see if the medication you are using is a covered drug.

If you are administered medication or drugs by a health care provider at a clinic, doctor’s office, or outpatient facility, your medication will fall under Medicare Part B.

Original Medicare, Medicare Advantage, and Part D

Part D expenses aren’t covered by Original Medicare (Part A and B) because prescription drug coverage is a separate Medicare insurance category.

If you have Original Medicare, you can get a stand-alone prescription drug plan or a Medicare Supplement Plan (Medigap) to cover your prescription drug expenses.

It’s best to check with your insurance provider or the CMS (Centers for Medicare and Medicaid Service) if you are already covered for Part D expenses with your current plan.

You won’t be able to get a stand-alone Part D plan if you have Medicare Advantage. Most Medicare Advantage (Part C) plans offer prescription drug coverage. If you’re enrolled in a Medicare Advantage plan, you'll probably have some kind of prescription drug coverage.

Part D insurance plans offer different tiers of coverage that will provide different degrees of insurance for medical costs. You’ll be able to choose your tier of coverage on standalone Medicare Part D plans and Medicare Advantage plans.

(Source: Pexels)

What Expenses Will Medicare Part D Plans Cover?

According to federal regulations, all Medicare Part D plans must cover a wide range of prescription drugs or medicines that Medicare enrollees use.

Depending on your tier of coverage and Part D provider, you may not have to pay anything towards the costs of your drugs or prescription medication.

However, if you are on a more affordable type of plan there may be out-of-pocket costs that you will have to pay when you use your Medicare Part D cover.

Each Medicare Part D insurer will have a different list of covered drugs (also known as a “formulary”), so it’s best to check with each provider to see what drugs they will pay for before signing on to a plan.

Prescription medications such as blood pressure pills, statins, heartburn tablets, and certain types of vaccines like the shingles vaccine will be covered under your Medicare Part D drug plan.

However, you may need to get authorization from your plan provider. In other cases, you may have to substitute your medication for generic drugs on your Medicare drug plan’s approved list.

For example, your Medicare provider may not cover a well-known antidepressant such as Zoloft, but it may cover the generic compound (Sertraline Hydrochloride).

The best way of finding out what you’re covered for is by contacting your provider and requesting a formulary list from them. If you have any questions, speak to your Medicare Part B coverage provider and find out what tiers of coverage they offer and how they will affect you.

You Can Request Changes to Your Part D Coverage

If you feel that your plan should cover a specific prescription medication, there’s always the option of requesting an exemption or revisement of your approved medicine list.

Speak with a PolicyScout consultant to learn more about how you can approach these situations.

How Do I Enroll for Medicare Part D?

If you have an Original Medicare plan, some private insurance companies offer stand-alone Part D cover. These are also known as Medicare Drug Plans or Medicare Prescription Drug Plans.

If you are enrolled in a Medicare Advantage plan (Part C), you will probably have some type of coverage for Part D expenses already and are not allowed to sign up for a stand-alone Medicare Drug Plan.

Be sure to have both your Medicare and Social Security cards on hand when you fill out your application form. Before you sign up, you’ll have to be registered for Medicare Part A to qualify for Part D cover.

You will also need to provide your Social Security information in your application form. Remember that your Social Security details are confidential, and never give out your Medicare or Social Security information over the phone.

If you need some help with finding a great Part D health care provider or would like to know more about Part D coverage in your area, reach out to our team of knowledgeable agents with your questions.

What Does It Cost to Enroll in Part D?

The monthly cost of enrolling in Medicare Part D will depend on two things: your plan’s premiums and your income-adjusted rate.

In general, providers will offer different plans or “tiers” of coverage that offer varying coverage based on your monthly premiums.

If you opt for a lower-cost plan, your coverage options may be less than what you would have on a higher-tier plan. The average monthly premium for stand-alone Part D coverage in 2021 was $33.00 per month.

The Income-Related Monthly Adjustment Amount (Part D-IRMAA), which is based on your previous year’s tax returns, might increase your monthly enrollment costs between $12.30 and $70.70 based on your filed tax return amount.

You will also have to pay an annual “deductible cost,” which is the amount you need to pay before your Part D coverage begins. This can range between $100.00 and $445.00 per period of cover depending on your plan.

Find Out What Your Estimated Monthly Cost Will Be with Different Income Adjustment Monthly Amounts

Part D Income Adjusted Monthly Rates for 2022 based on your 2020 income

| File individual tax return | File joint tax return | File married & separate tax return | You pay each month (in 2022) |

|---|---|---|---|

| $91,000 or less | $182,000 or less | $91,000 or less | your plan premium |

| above $91,000 up to $114,000 | above $182,000 up to $228,000 | not applicable | $12.40 + your plan premium |

| above $114,000 up to $142,000 | above $228,000 up to $284,000 | not applicable | $32.10 + your plan premium |

| above $142,000 up to $170,000 | above $284,000 up to $340,000 | not applicable | $51.70 + your plan premium |

| above $170,000 and less than $500,000 | above $340,000 and less than $750,000 | above $91,000 and less than $409,000 | $71.30 + your plan premium |

| $500,000 or above | $750,000 or above | $409,000 or above | $77.90 + your plan premium |

(Source: Medicare.gov)

For example, if you filed a tax return in 2019 of between $91,000.00 and $114,000.00 you would have to pay your quoted monthly premium (for example, $65.00) plus a $12.40 income adjustment fee. This would bring your total to $77.40 per month.

But if you filed a tax return of $500,000 dollars in the same period you’d have to pay a $77.90 income adjustment fee, bringing your total to $142.90 per month.

If you’re unsure about choosing a Part D provider, shop around and compare the different plans on offer in your state. PolicyScout has put together a list of the best Medicare providers in the country and would be happy to walk you through your different healthcare options.

Medicare Part D Plan Coverage Costs

Part D plan costs consist of:

Your monthly premium.

An income-adjusted rate based on your tax return.

An annual deductible cost.

For example, if you choose a mid-tier plan ($33.00) and filed a tax return above $111,000.00 for the previous year you would pay $777.60 ($64.80 per month) plus an annual deductible of $445.00, bringing the total cost of Medicare Part D coverage for that year to $1,222.60.

Out-of-Pocket Expenses and Medicare Part D

Medicare Part D drug plans won’t cover 100% of your prescription medication costs, and some drugs may not be covered by your Medicare Part D provider based on their medication formulary or approved drug list.

Another issue that causes financial headaches for many Medicare beneficiaries is that there is no limit to out-of-pocket expenses.

Coverage Thresholds for Part D Plans in 2022

Initial Coverage Limit The amount of coverage your Part D plan will provide before you reach your coverage gap.

Coverage Gap Threshold: $4,430.00 Your Part D plan will cover 75% of the costs of your medication once you reach this threshold. You will have to pay 25% of your prescription costs.

Catastrophic Coverage Threshold: $7,050.00 Your Part D plan will not cover any expenses over this amount for the remainder of your coverage period. You will have to pay 100% of the expenses.

Most Medicare Part D plans have a coverage gap threshold which temporarily limits the amount you can spend on prescription medicines through your Part D plan.

If either you or your plan’s spending on drug costs exceeds your initial coverage limit, you’ll be placed in the coverage gap.

If this happens, you might be limited to certain brand names of medicines by your Part D plan and you will have to pay 25% of the cost of your prescription medicine.

Part D plans also have a “catastrophic coverage threshold” which limits the amount of coverage you will get each year through your Part D provider. For 2022, the threshold is set at $7,050.00.

This means that if your prescription medication costs go over the catastrophic coverage threshold for the coverage period, you would be liable for all the costs for the medicine you’ve purchased.

For example, if you were taking medication for Alzheimer’s or leukemia and you reached the $7,050.00 catastrophic coverage threshold four months into the year you would be liable for all your Part D costs for the last eight months of the year.

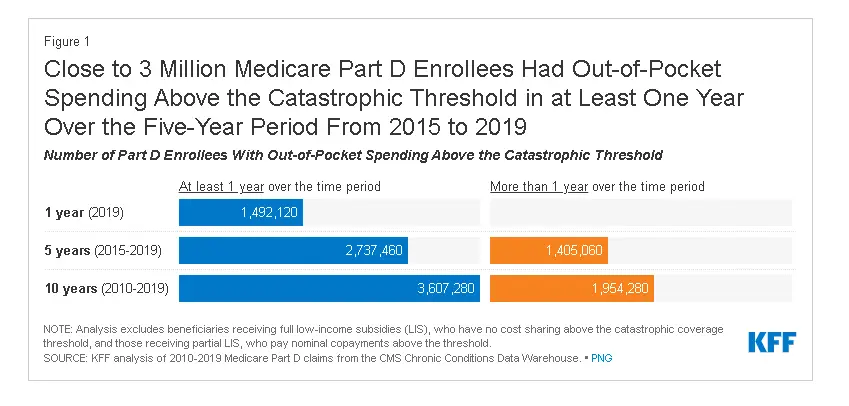

The Number of People Who Exceed Their Part D Threshold Is Larger than You Might Think

The Kaiser Family Foundation estimates that nearly 3 million Medicare Part D enrollees reached their catastrophic threshold in at least one year of Medicare cover between 2015 and 2019. (Source: KFF)

This can be worrying for many people who suffer from diseases that require costly interventions and treatments.

In most cases, people who aren’t on a Medicare Advantage plan will sign up for a Medigap plan that will help cover their Part D expenses.

These plans are a great way of limiting your medical liability and providing protection against expensive prescription medicine costs.

If you’d like to learn more about the different Medigap options, A-N, feel free to speak to a consultant from PolicyScout who will walk you through the other plans.

Finding the Right Medicare Plan Can Be Difficult

If you’re thinking about getting Part D coverage, you’ll first have to find a plan that suits your circumstances and needs.

At PolicyScout, we’ve reviewed Part D plans from across the U.S. and found the best providers for Medicare Part D and Medigap coverage.

If you're interested in learning more about reliable Part D plans and providers in your area, give our team of Medicare consultants a call.

What Do I Do If I Haven’t Paid Medicare Taxes?

Medicare drug coverage is funded by monthly premiums, so your Medicare tax contribution history won’t affect the cost of your coverage.

You may, however, be subject to a late enrollment fee if you have chosen not to use a Part D plan and want to sign up after the initial enrollment period.

This fee is calculated on the period of time that you went without coverage and is set at 1% of the national base premium (the average cost of Medicare Part D for the current plan year).

For example, if you haven’t had any form of Part D coverage for 12 months your penalty will be 12% of the base premium ($33.06), which will give you a penalty of $4.00 per month ($3.96 rounded to the nearest $0.10).

Unfortunately, you will have to pay this penalty for as long as you have a Medicare drug plan, but you can always ask your provider to reconsider it if you have a reason for not enrolling while you were eligible.

How Do I Find Out More about Part D Healthcare Coverage?

At PolicyScout, we provide up-to-date information and articles about Medicare, Medigap plans, and health insurance. If you want to learn more about your Medicare coverage options, visit our Medicare hub or browse through our articles on Part A, Part B, and Part C.

If you have any questions or would like to find out about the federal Medicare program, Part D plans, or Medigap providers in your area, feel free to contact us at 1-888-912-2132 or email us at Help@PolicyScout.com.

FAQs about Medicare Part D

Will Medicare Part D cover all of my prescription drug expenses?

Depending on your specific Part D plan, you may get coverage for all your prescription drug costs. However, you also might be liable for copayments and out-of-of pocket expenses if you exceed the threshold of coverage for your current period.

How do I enroll for Medicare Part D cover?

If you are part of a Medicare Advantage plan (Part C) you will probably have Medicare Part D coverage. If you are using Original Medicare, you can enroll in a standalone Part D plan through a private insurer. Find a Part D provider, apply for coverage, and contact them to find out when your cover starts.

What will Medicare Part D coverage cost me?

Stand-alone Medicare Part D plans range between $10.00 and $100.00 per month depending on your tier of coverage. You’ll also have to pay an income-adjusted rate that is based on your submitted tax return for the previous tax period.

What vaccines will be covered under Medicare Part D?

Vaccines for shingles and tetanus are covered under Medicare Part D. The Covid-19 vaccine is covered under Medicare Part B.

What is the catastrophic threshold for Medicare Part D expenses?

In 2022, the catastrophic threshold for Medicare expenses is $7,050.00. If your medication costs exceed this, you may be liable for copayments or the total cost of the medicines you use.

When can I enroll for Medicare Part D?

You can enroll in Medicare Part D three months before and three months after the month of your 65th birthday. You can also sign up during the general enrollment period between January and March if you are over 65.