How Does Medicare Work in 2022? A Guide to Understanding Medicare Health Coverage.

Find out what Medicare is, how to apply, what is covered by the different plans, and how you can benefit from enrolling.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

More retirement-age people are interested in finding out about the medical insurance options that the government provides.

It’s essential to understand the benefits, options, and obligations around Medicare, as well as the potential gaps in coverage that could have a long-lasting impact on your bank account and your overall quality of life.

The complex nature of the Medicare system, along with its complicated terms, payment options, and requirements can leave you scratching your head and wondering where to turn.

At PolicyScout, we’ve made it our mission to sort through the jargon to provide you with clear and easy-to-understand information on health coverage in the U.S.

That’s why we’ve created this comprehensive article to define Medicare, address common questions about the federal U.S. health insurance program, and help you decide on your healthcare options in 2022.

Facts about Medicare and healthcare in America

What is Medicare?

More and more people are signing up for Medicare each year, with enrollment reaching a twenty-year high in 2021. But there’s still much confusion around what the program is and how it can benefit Americans.

Medicare is a federal health insurance program that provides affordable healthcare and subsidizes the cost of treatments, medicine, and medical services for people living in the U.S.

Medicare is not the same as Medicaid, which is the federal healthcare plan for lower-income individuals. Instead, Medicare assists senior citizens and other groups who need assistance with their medical costs as they progress through life.

If you live in the U.S. and are nearing retirement age (65 or older), are a younger person with disabilities, or suffer from certain conditions like ESRD (End-Stage Renal Disease), you are eligible for Medicare.

For example, if you’ve worked for most of your life, are near retirement age, and paid your taxes, you’ll be able to sign up online for Medicare through the Social Security Agency (SSA).

Social Security and Medicare

Did you know? If you’re receiving Social Security benefits, you’re already enrolled in Medicare and should contact the SSA to learn how to get started using your plan.

If you are turning 65 in the next three months but don't want to use your Social Security benefits just yet, you can still sign up just for Medicare through the SSA website.

How does Medicare work?

When you enroll, you’ll receive a Medicare card linked to your Social Security number. This card will allow you to receive medical treatment and services at discounted rates in public hospitals and other approved medical facilities.

You’ll be able to get medication, medical advice, and the medical assistance you need at subsidized rates of up to 80% of the original cost.

This can include operations, doctor consultations, medication, medical tests, ambulance services, or even visits to the physiotherapist or chiropractor.

It’s important to note that while you may sign up for Original Medicare through the Social Security Agency, your Medicare coverage is different from your Social Security.

Your Social Security Card vs. Your Medicare Card

What does Medicare cover?

If you’re asking yourself the question, “What does medicare pay for?” the short answer is that it will cover some of the costs for most legitimate medical expenses.

As long as your medical treatment is on the approved list, you’ll be able to claim the Medicare discounted rate on the service you’ve used.

If you’d like to find out more, here’s a great resource provided by the Social Security Agency to find out what different outpatient procedures will cost through Medicare.

Another way of finding out if Medicare covers procedures, medication, or services is simply talking with your doctor, nurse, or healthcare provider and asking if Medicare covers their services.

Making sense of the different types of Medicare

The government’s Medicare program aims to offer eligible people affordable healthcare options as they get older.

Medicare covers hospital or “inpatient” insurance (Part A), general medical or “outpatient” insurance (Part B), and self-administered prescription drug coverage (Part D). The three Medicare programs have unique costs, benefits, and criteria for enrollment.

It can all get a bit complex if you don’t know what each part covers or what you should do to get your benefits.

To help you make sense of it all, we’ve put together a brief overview of the different sections of Medicare and what it costs to use it.

What is Medicare Part A?

Let’s start with the most significant part of the federal health program — Medicare Part A. Medicare Part A concerns the care and treatment of people in hospitals or registered medical facilities.

For example, you’ll get portions of hospital-related stays and expenses covered or subsidized when you sign up for Medicare Part A.

Medicare Part A insurance will include surgeries, specialist consultations, inpatient care, and most treatments performed in hospitals. Medicare Part A also covers certain types of outpatient care at registered nursing facilities.

Part A would not cover the prescription medication you use at home or mental health consultations. These medicines and other outpatient therapies would fall under Part B and Part D expenses.

Most citizens aged 65 or older who have paid Medicare tax for at least ten years can sign up for Medicare Part A at no cost and use the program to reduce their treatments and medical care bills.

Medicare Part A Costs

If you’ve paid Medicare taxes for at least ten years or forty financial quarters, you won’t have to pay monthly premiums to enroll in Medicare Part A.

If you haven’t contributed towards Medicare through a payroll tax there may be a monthly premium, ranging between $274.00 and $499.00.

Something to remember is that penalties start at 10% of your monthly premium for each year (65+) you haven’t enrolled in Medicare Part A.

What is Medicare Part B?

Medicare Part B covers outpatient care and services, including bills for consultations with specialists, rehabilitation costs, and physical therapy.

Part B expenses can also include preventative services, doctor visits, mental health costs, and some prescription medications. It can also cover ambulance rides, blood pressure medication, and cholesterol tablets.

For example, if you consult with a physiotherapist this would be part of your outpatient care and services.

Or if you need to go to the hospital in an ambulance because of a medical emergency, this service would fall under Medicare Part B expenses.

Outpatient coverage (Medicare Part B) is optional, as monthly premiums and costs can fluctuate depending on income, tax history, and marital status.

Ultimately it’s up to you to decide whether you enroll in Part B, but just remember there are associated penalties if you decide against it.

Medicare Part B Costs

The monthly cost of Medicare Part B can start at around $170.10, and coverage usually means that you will pay 20% of the approved costs for services in this category of medical care.

For example, if a procedure usually costs $1000.00, with Medicare Part B you’d pay $200.00 and Medicare would pay the difference.

What is Medicare Part C?

Medicare Part C, now known as Medicare Advantage, is the umbrella term for medical insurance plans that cover Part A (Inpatient), Part B (Outpatient), and Part D (Self-administered Prescription Medication) costs.

These plans are privately run health insurance policies that offer various payment options, coverage, and additional benefits.

Many Medicare Advantage plans also cover non-prescription medications and other therapies not covered by the Original Medicare framework.

If you’d like to know more about some well-known Medicare Advantage plans, feel free to send us an email or check out PolicyScout’s Medicare Hub.

Medicare Part C (Medicare Advantage) Costs

The prices and costs associated with each plan will vary significantly. Based on plan benefits, copayments options, and coverage, you might pay no premium or up to a couple of hundred dollars every month.

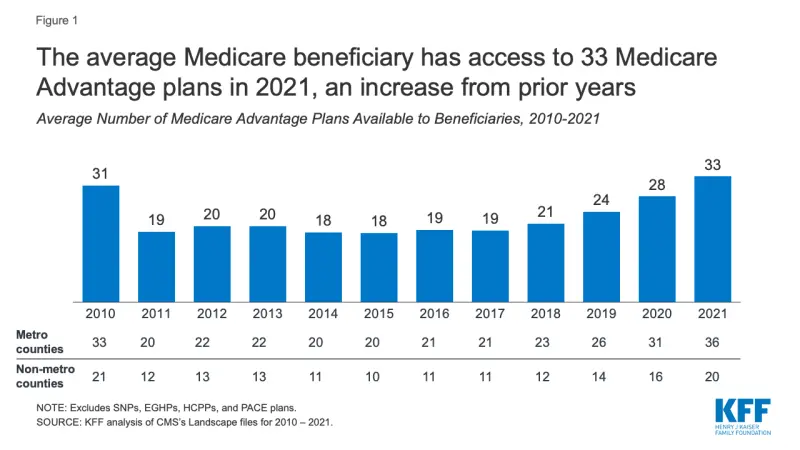

The number of Medicare Advantage plans has boomed in the past four years:

Today there are more Medicare Advantage plan options available to eligible enrollees than in the last ten years. PolicyScout’s expert advisors can help you navigate your choices. (Source: KFF)

What is Medicare Part D?

Medicare Part D covers costs relating to prescription drugs that aren’t administered to you by a registered health professional in a medical facility. These can include medication for pain, antibiotics, anti-inflammatories, and other medications.

For example, if you go to the doctor because you’ve been experiencing back pain or trouble sleeping, the cost of the medication they prescribe you will fall under Medicare Part D costs.

Prescription medication means drugs that are prescribed to you by a qualified and registered medical doctor. Treatments such as herbal remedies, Eastern medicine, or homeopathy are unfortunately not covered by Medicare.

Because Medicare Part D isn’t government-administered, you’ll be happy to know that there are hundreds of private companies that offer Medicare Part D plans across the U.S. Each state has different providers with unique plan options and prices.

Our advice is to use this to your advantage. Shop around and find a coverage option that suits your individual needs and circumstances.

If you want to learn more about the different Part D policies available in your state, reach out to one of our consultants to discuss how you can get prescription coverage.

Medicare Part D Costs

Medicare Part D monthly plans start at around $32.00, with more comprehensive plans (with enhanced benefits) costing approximately $44.00 per month. Here’s an article to help you determine what you would pay for prescription medicine cover with Medicare.

Types of coverage plans for Medicare

As an eligible Medicare recipient, two broad basic Medicare options are available to you — Original Medicare and Medicare Advantage.

Original Medicare is government-run and covers costs associated with Part A and Part B expenses. Medicare Advantage, previously known as Medicare Part C, is offered by private companies and takes care of Part A, Part B, and Part D expenses.

On top of this, you also get supplemental insurance plans (Medigap) that cover shortfalls in Medicare. There are a few types of Medigap plans available, and these are known as Plans A to N.

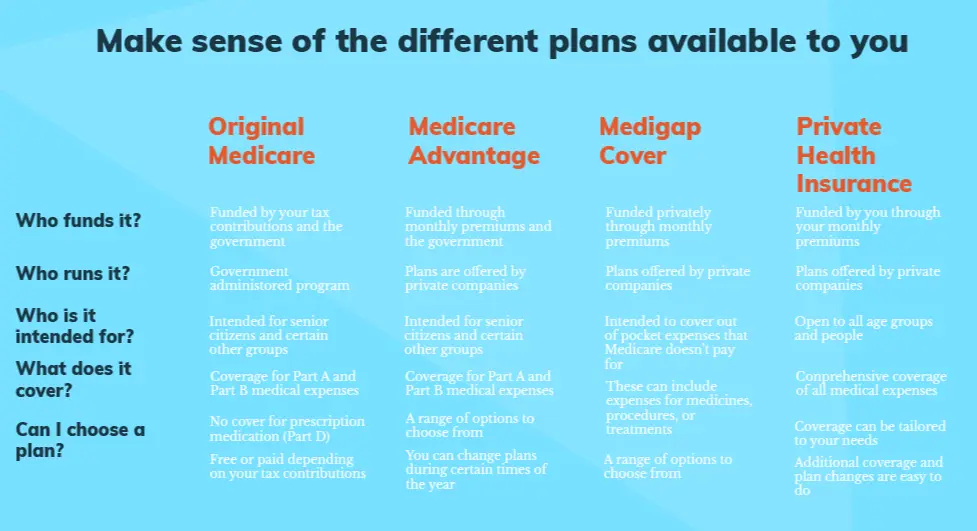

Some people choose not to sign up for Medicare and use private health insurance to pay for their medical expenses. Take a look at this infographic we’ve put together to help explain the difference between the types of coverage available.

How do I enroll for Original Medicare and Medicare Advantage?

If you’re thinking about signing up for Medicare or just want to know more about the enrollment process, we’ve laid out the steps for you here.

You can sign up for Original Medicare through the Social Security Agency website or by phoning them at 1-800-772-1213.

Just remember that you’ll have to create a my Social Security Account. If you’re unsure, it’s best to call the SSA and get someone to assist you.

Once you’re registered, the SSA will provide you with a Medicare card that has your name, social security number, and the nearest treatment facility in your area on it. This process should take around two weeks.

What you should know about Medicare enrollment and penalties.

If you or your employer have not paid Medicare taxes, you may be liable for a monthly premium to fund your enrollment into the Medicare program.

The technical requirement is that you must have contributed towards the Medicare program through Medicare Tax for at least ten years or 30 financial quarters.

There are also penalties if you willingly decide not to enroll in the Medicare plan. Be sure to check with your health insurance provider or the Social Security Agency to see how you can prevent or minimize these penalties through a Medicare Advantage plan.

There are resources to help you minimize the financial burden of joining Medicare after 65, such as Special Enrollment Periods. The best way of finding out where you stand is by speaking to a health insurance professional or the SSA about your Medicare status.

What kind of treatments aren’t covered by Medicare?

A big concern for people in their golden years is maintaining their quality of life and health. But unfortunately, Original Medicare doesn’t cover all medical treatments or procedures.

For example, cosmetic and dental procedures aren’t covered by Original Medicare and this can mean you’ll have to foot the bill for things like hearing aids, tooth removals, and dentures.

Or if you want to go for specific eye exams, undergo acupuncture treatment, or need routine foot care, Original Medicare won’t always cover these costs.

Original Medicare plans don't cover medical expenses incurred overseas, so if you plan on traveling in your golden years this is something to consider.

With medical expenses adding up quickly, there is no telling what specific treatments, medications, or procedures you may need to ensure your good health over time. The great thing is that you can supplement your Medicare with other insurance plans, such as Medigap cover.

Use this Medicare coverage list provided by the U.S. government to determine whether your medical test, item, or service falls under claimable Part A or Part B expenses.

We’ve also got a list of the top Medigap insurance plans in your state if you’re thinking about supplementing your Original Medicare or Medicare Advantage plan.

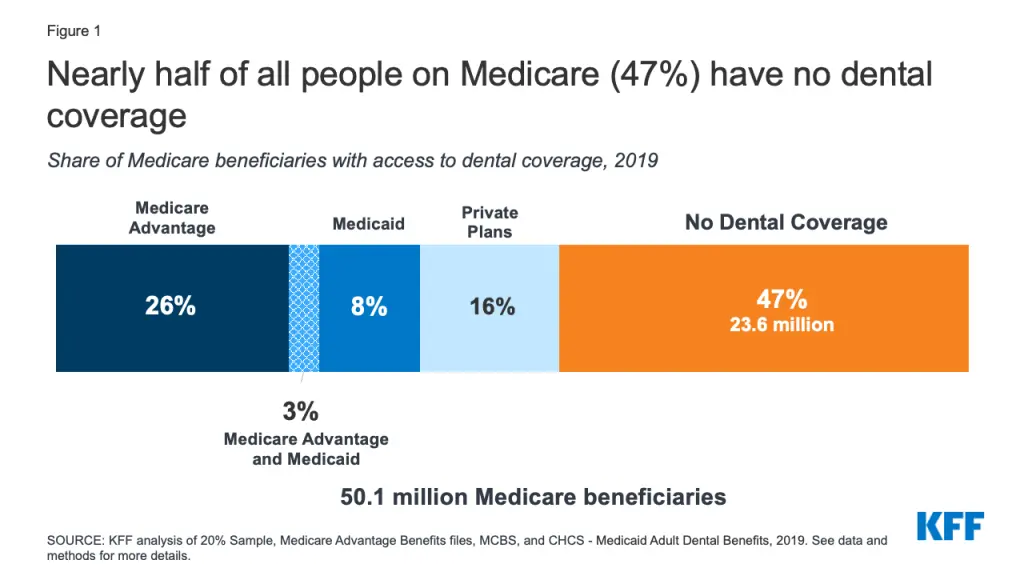

As seen in this KFF analysis, nearly half of all Medicare members don’t have dental coverage. Our advice is to be aware of the limits of your plan when you sign up and to plan for shortfalls in your cover with a reputable Medigap plan.

Should I get health insurance on top of Medicare?

If you are in good health and have a Medicare-approved hospital or facility nearby, you will benefit from signing up for the federal government’s health insurance program.

But you should be aware that with Original Medicare and even specific Medicare Advantage plans, you won’t always get all the personal medical insurance benefits you’re used to.

Many senior citizens would also like to have a say in the standard of treatment, medicines, and medical services they get.

If you’re facing this dilemma, you’ll be happy to know that you have a few options through Medicare Advantage and other private medical schemes.

Generally speaking, people will opt to purchase comprehensive insurance through (Medicare Advantage), private medical insurance, or even Medicare Supplement (Medigap) cover. Feel free to look at our list of top providers for Medicare Advantage and Medigap plans.

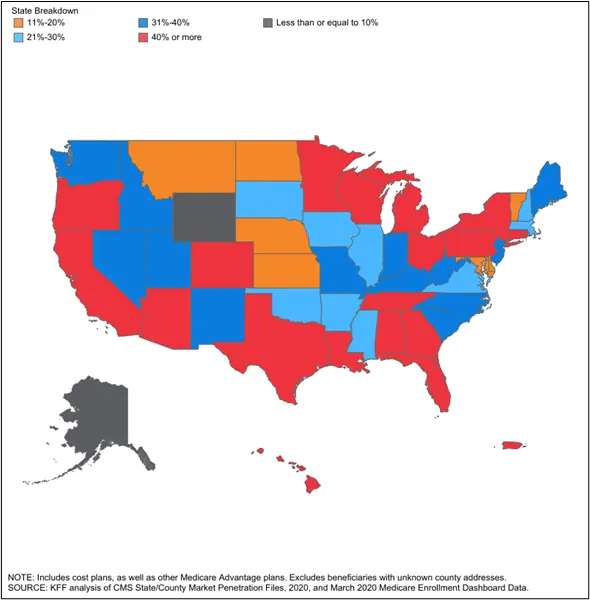

Medicare Advantage Uptake in the U.S. by State in 2020

This map of the U.S. shows the number of people who have signed up for a Medicare Advantage Plan in 2020. With 71 million Americans turning 65 by 2030, this figure is expected to rise in the coming years. (Source: KFF)

Find out more about health coverage options in your area.

At PolicyScout, we pride ourselves on our ability to give clients market-leading advice about their medical insurance options.

If there’s something you’d like to learn more about or you have a question about your medical coverage, our consultants are ready to assist.

Reach out to one of our agents to discuss comprehensive health insurance programs and medical gap cover options today.

Some top tips to help you learn more about your Medicare benefits:

Find out if your employer or your spouse’s employer has been paying your Medicare taxes.

Contact Social Security to determine whether you qualify for Medicare Part A, Part B, or Part D.

Speak to your healthcare insurer to determine your coverage for non-qualifying procedures, treatments, and services.

Get a range of quotes from a trusted source to find the best Medicare Advantage plan in your state.

Find out whether or not you’re subject to a penalty fee or permanently higher premiums based on your income or non-enrollment status.

Some helpful external links:

The Social Security Agency: https://www.ssa.gov/benefits/medicare/

The Official Medicare government website: https://www.medicare.gov/

The National Council on Aging - https://www.ncoa.org/article/medicare-part-d-cost-sharing-chart

Medicare FAQs

What is Medicare?

Medicare is the federal health insurance program for senior citizens and certain disabled groups. Tax contributions, monthly premiums, and the federal government fund the plan.

What is Original Medicare?

Original Medicare is the term for Medicare Part A (Inpatient) and Medicare (Outpatient) coverage. Original Medicare subsidizes hospital costs like surgeries and out-of-hospital expenses such as doctor consultations. Original Medicare doesn’t cover prescription medications.

What is Medicare Advantage?

Medicare Advantage used to be called Medicare Part C and refers to private health plans that cover inpatient (Part A), outpatient (Part B), and prescription medicine (Part D) expenses.

Is Medicare the same as Medicaid?

No, Medicare is not the same as Medicaid. Medicare is the federal health insurance plan for Americans nearing or in retirement (65+). Medicaid is the federal health program for low-income people who require affordable healthcare solutions.

How much will it cost to enroll in Medicare?

The price for enrolling in Medicare will vary depending on which Medicare plan you have, plus other factors like your tax contributions to the scheme and enrollment history. You might have to pay a monthly premium if you haven’t contributed to Medicare through taxes for at least ten years.

Who can enroll in Medicare?

Any person nearing the age of 65 can register for Original Medicare through the Social Security Agency. If you have a disability or other chronic medical condition (like ESRD) and are under 65, you can also sign up for the program.

When can I enroll in Medicare?

You can enroll in Original Medicare upon turning 65. There’s a seven-month window for you to complete your initial enrollment — that’s three months before and after the month of your birthday.

How can I find out more about my Medicare options?

Visit the official government Medicare website, speak to the Social Security Agency, or reach out to an industry expert like PolicyScout to learn more about your Medicare and Medigap options.