When Can You Enroll in a Medicare Supplement Plan or Medigap Policy?

This article will cover when you can enroll in Medicare Supplement Plans and how to do it.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

If you’re thinking about joining a Medicare Supplement Plan or Medigap policy, figuring out when to enroll can be difficult.

While you can enroll in a Medicare Supplement Insurance at any time, if you enroll at the wrong time it can sometimes limit your choices, cost you more money, and affect your cover.

This article will discuss when you can enroll in a Medicare Supplement Plan and what you should know before you do.

What Are Medicare Supplement Plans?

Since 2014, nearly 4 million people have purchased a Medicare Supplement Plan. But what are they, and why are they becoming more popular for people on Medicare?

Medicare Supplement Insurance Plans, also known as Medigap plans, are health insurance policies for people who have Original Medicare cover.

Like Medicare Advantage plans, these policies help pay for the additional costs of Original Medicare services, items, and equipment, and some plans even offer prescription drug coverage.

As a member of a Medicare Supplement Plan, you will pay a monthly fee on top of your Original Medicare premiums and get additional coverage for costs that Original Medicare doesn’t pay for.

Who Is Eligible to Enroll in a Medicare Supplement Plan?

Anyone who is eligible for Original Medicare coverage can buy Medicare Supplement Insurance.

You can enroll in Original Medicare if you are 65 or older (or turning 65 in the next three months), have a disability, or suffer from ESRD (End-Stage Renal Disease).

If you’re wondering about whether you can sign up for a Medicare Supplement Insurance Plan, keep the following points in mind:

You must have both Medicare Part A and Part B to join a Medicare Supplement Plan.

You cannot have a Medicare Advantage plan or a standalone Medicare Part D plan.

Medicare Supplement Insurance policies only cover one person, so separate plans are needed if you want to cover another family member.

Medicare Parts Explained:

Medicare Part A relates to hospital insurance, inpatient care, home health care, and hospice care.

Medicare Part B has to do with outpatient or general medical care and includes blood tests, screenings, doctor’s visits, and preventive treatments.

Medicare Part C (known as a Medicare Advantage plan) are private health plans that cover Part A and B expenses and have additional benefits such as prescription drug cover, dental care, and vision care.

Medicare Part D helps to cover the costs of self-administered prescription drugs and is provided by private insurance companies.

When to Apply for Your Medicare Supplement Plan

Purchasing a Medicare Supplement Plan can be a stressful process, but signing up at the right time will ensure:

That your preferred plan provider accepts your application.

That you don't pay a higher premium because of preexisting medical conditions.

You will be able to enroll in a Medicare Supplement Insurance policy at any time. However, if you are new to the Medicare program your Medicare Supplement Open Enrollment Period is probably the best time to do it.

Medicare Supplement Open Enrollment Period

Your Medicare Supplement Plan Open Enrollment Period (also known as your Medigap Open Enrollment Period) is a one-time six-month period when you can sign up for a Medicare Supplement Plan without having to worry about your health status or chronic conditions.

The Medicare Supplement Open Enrollment Period begins the month you turn 65 and enroll in Medicare Part B.

This period is outlined by federal law and ensures that all first-time enrollees get equal treatment, options, and protection the first time they choose a plan.

During your Medicare Supplement Open Enrollment Period:

You will be able to buy any Medicare Supplement Insurance Plan that a health insurance company sells.

Companies will not be able to refuse to sell you Medicare Supplement Insurance policies during this time.

Insurance companies will not be allowed to perform medical underwriting.

Plan prices will be the same, regardless of your health status.

What Is Medical Underwriting?

Medical underwriting is the process where a health insurer reviews an applicant’s medical history to decide on membership, membership rates, and coverage.

Medicare Supplement Insurance Plans cannot perform medical underwriting on you if you are in your Medicare Supplement Open Enrollment Period (Medigap Open Enrollment Period).

(Source: Pexels)

Special Enrollment Periods and Medicare Supplement Plans

Usually, a person will only get one opportunity to benefit from their Medigap Open Enrollment Period.

However, depending on specific conditions you could also qualify for a Special Enrollment Period.

A Special Enrollment Period is a unique opportunity for people in particular circumstances to get an Open Enrollment Period a second time.

For example:

If you enroll in Part B, go back to work and join your employer’s healthcare coverage. You’ll get a second Medicare Supplement Open Enrollment Period when you retire again.

If you are eligible for Medicare due to a disability and signed up before the age of 65. You’ll get two Medicare Supplement Open Enrollment Periods. One when you initially enroll for Part B cover and another when you turn 65.

Applying at Any Time for a Medicare Supplement Plan

You can also purchase Medicare Supplement Insurance outside of your Medicare Supplement Open Enrollment Period, but remember that insurance companies don’t have to accept you as a member.

Your medical history will also be reviewed, which might mean you will not be accepted onto the plan or that the cost of enrolling could be more than you would pay during your Open Enrollment Period.

Your provider might implement a waiting period for chronic or preexisting conditions coverage (also known as a Preexisting Condition Waiting Period).

What Are Preexisting Condition Waiting Periods?

Pre-existing Condition Waiting Periods are how Medicare Supplement Insurance providers ensure they aren’t unknowingly enrolling people with high medical expenses.

They do this to protect their current members from price changes and ensure their plan isn’t put under financial strain by new members with expensive treatment needs.

Waiting periods can last up to six months, and during this time Medicare Supplement Insurance Plans do not pay for costs relating to preexisting conditions.

For example, if you have high blood pressure and you enroll outside of your Medicare Supplement Open Enrollment Period, your Medicare Supplement Insurance provider might refuse to cover your medication and treatment costs for the first six months of your membership.

However, there is an exception to this. If you have guaranteed issue rights, you can purchase a Medicare Supplement Plan without any of the risks covered above.

When will you have guaranteed issue rights?

Guaranteed issue rights mean that an insurance company must:

Sell you a Medicare Supplement Insurance policy.

Cover all of your preexisting conditions.

Not charge you more for a policy because of your current or previous health conditions.

You will qualify for guaranteed issue rights when:

Your insurance company stops offering coverage where you live.

A union payment plan you are part of ends.

You change from a Medicare Advantage plan back to Original Medicare coverage in your first year of enrollment.

You leave a Medicare Supplement Insurance Plan for a Medicare Advantage plan but decide to swap back to Medicare Supplement Insurance in the first year of enrollment.

(Source: Pexels)

Be sure to check the Medicare Supplement Insurance regulations in your state.

Medicare Supplement Insurance Plans are standardized across the U.S. to ensure that everyone gets the same essential benefits and coverage.

However, the three states below have unique rules and regulations.

Wisconsin

Minnesota

Massachusetts

If you live in these states, check with your local Social Security Agency or Medicare Supplement Insurance provider to see how this will affect you.

Further Learning: PolicyScout's Guides To Medicare Supplement Plans By State

For more information about the most popular Medicare Supplement Plans by State in the U.S., check out the following guides:

The Ulitmate Guide to Medicare Supplement Plans in Florida

The Ultimate Guide to Medicare Supplement Plans in Georgia

The Ultimate Guide to Medicare Supplement Plans in North Carolina

The Ultimate Guide to Medicare Supplement Plans in Ohio

The Ultimate Guide to Medicare Supplement Plans in Pennsylvania

Choosing the Right Medicare Supplement Plan Can Make All the Difference.

It’s also important to consider the type of cover you get when you sign up for a Medicare Supplement Plan.

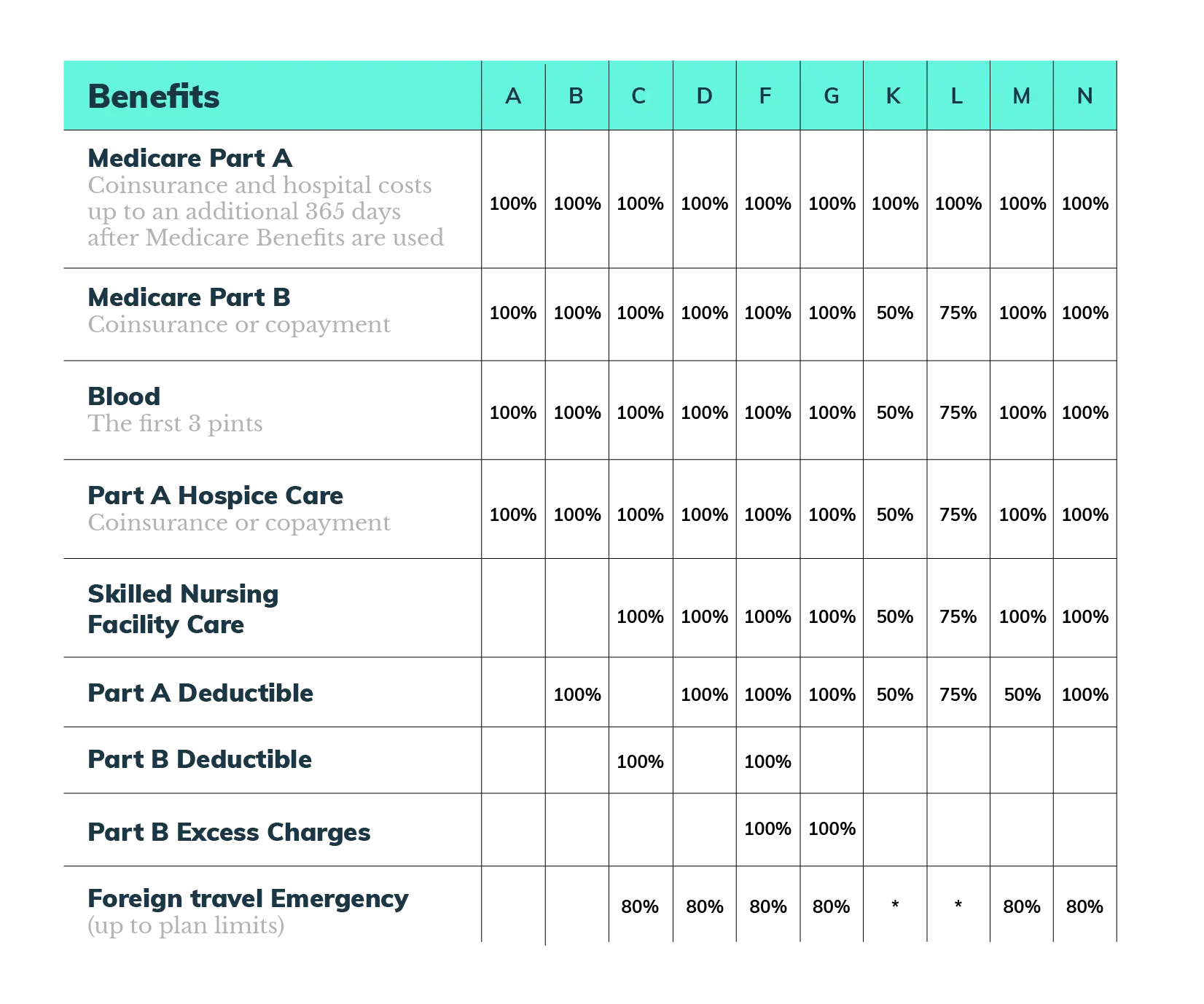

There are ten kinds of Medicare Supplement Plans, ranging from A-N. Each plan has unique coverage options and insurance companies can charge different rates depending on your location and their pricing structure.

Further Learning: PolicyScout's Breakdown of Medigap Plans A-N

Check out or quick breakdowns of each Medigap plan and what they cover

| Type of Medicare Supplement Plans | |

|---|---|

| Medigap Plan A | Medigap Plan G |

| Medigap Plan B | Medigap Plan K |

| Medigap Plan C | Medigap Plan L |

| Medigap Plan D | Medigap Plan M |

| Medigap Plan F | Medigap Plan N |

Coverage for costs and out-of-pocket expenses depends on the plan you choose, and often people don’t know what benefits they are getting.

Key Terms to Remember When Choosing a Medicare Supplement Plan:

Coinsurance - The amount a Medicare beneficiary will have to pay for healthcare services, items, and equipment.

Deductibles - The amount that a Medicare enrollee will have to pay each coverage period towards expenses before their Medicare coverage starts.

Copayments - Set amounts that Medicare beneficiaries pay for medical services and items, such as doctor’s consultations and blood tests.

Monthly premiums - The amount that Medicare enrollees have to pay each month for Medicare coverage for Part and B expenses.

Out-of-pocket expenses - These are any costs that Medicare doesn’t cover, which a beneficiary must pay.

Before you decide on a plan, make sure that you’re getting the right cover for your medical costs and that your provider is offering a deal that's right for your needs.

Below is a table summarizing the different benefits that each plan covers. The percentage indicates how much coverage each Medicare Supplement Plan offers.

(Source: Pexels)

How Can I Learn More about Medicare Enrollment Periods?

Learning about different enrollment periods for Medicare Supplement Insurance, Medicare Advantage, and Original Medicare can be overwhelming and it's hard to know which rules apply to you.

The official government Medicare website is a good source of information for enrollment periods and other topics like Medicare Advantage plans and Part D drug coverage.

You can also visit PolicyScout’s Medicare Hub to learn more about Medicare in general, a specific Medicare Advantage plan, and Medicare Supplement Insurance plans.

We’ve made it our mission to make health care insurance and coverage easy to understand for everyone.

If you would like to learn more about the federal Medicare program, a Medicare Advantage plan in your area, or your health coverage options, reach out to one of our consultants by telephone or send us an email.