The Ultimate Guide to Medicare Supplement Plans in Ohio

Read on to learn more about how seniors in Ohio manage their out-of-pocket Medicare expenses.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

The federal Medicare program offers over-65s, people with End-Stage Renal Disease, and those with ALS (Lou Gehrig’s) access to more affordable health care across the nation.

But Medicare doesn’t cover all medical expenses. That’s why some people turn to private medical insurance plans, like Medicare Advantage plans or Medicare Supplement Insurance, to get additional coverage.

This article will go over Medicare Supplement Plans in Ohio, when the best time is to apply, which plans are the most popular, and how much you can expect to pay.

Let’s Recap: What Are Medicare Supplement Plans?

A Medicare Supplement Plan (also known as Medigap Plans) is health insurance coverage offered by private health care companies.

These plans offer specific benefits to help seniors pay for the remaining out-of-pocket costs that Medicare Parts A and B don’t cover.

People with Medicaid or a Medicare Advantage Plan cannot buy a Medicare Supplement Plan.

There are 12 standardized Supplement Plans in Ohio that private insurance companies can sell:

Each plan can be identified by a letter: A, B, C, D, F, G, K, L, M and N.

There are also two high-deductible plan options for F and G. These plans charge lower premiums but have a high deductible cost ($2,370 in 2021).

Supplement Insurance plans are the same across 47 states, which means that if you join Plan N in Ohio you’ll get the same health care benefits as a person in Georgia or California.

However, Wisconsin, Minnesota, and Massachusetts have their own plan types with different benefits.

Terms You Need to Know:

Deductible: An amount you have to pay before your insurance begins to cover health care services.

Coinsurance: The percentage of costs you need to pay for medical expenses such as tests, services, and items.

Copayment: Fixed amounts you will have to pay for doctor visits, hospital stays and prescriptions. These are set by your health insurance provider.

Out-of-pocket expenses: These are costs that aren’t covered by Medicare plans or private health insurance.

The amount of coverage you receive will depend on which Medicare Supplement Insurance Plan you choose.

Each plan will generally cover these kinds of expenses:

Your deductibles: The amount you have to pay before your insurance plan covers medical expenses.

Coinsurance: The portion of medical costs that you must pay (for Part B, this is 20% of the costs).

Other additional medical costs: This can include excess charges, blood transfusions, and foreign emergency cover, which Original Medicare doesn’t cover

Take a look at our Guide to Medicare Supplement Plans if you’d like to learn more about Medicare Supplement Insurance.

Key Takeaways:

Medicare Supplement Plans are also called Medigap plans.

Medicare Supplement Insurance helps cover health care costs that Original Medicare Part A and B don’t pay for.

There are ten different Medicare Supplement Plans you can choose from in Ohio. They can be identified by a letter: A, B, C, D, F, G, K, L, M and N.

If you already have Medicaid or a Medicare Advantage Plan, an insurance company cannot sell you a Supplement Plan.

When Is the Best Time to Enroll in a Medicare Supplement Plan in Ohio?

You can enroll for Medicare Supplement Plans in Ohio throughout the year. However, the recommended time to do it is during your Open Enrollment Period.

During your Open Enrollment Period, you’ll likely get better Medicare rates, have more options available to you, and you will not need to go through medical underwriting.

What Is Medical Underwriting?

Medical underwriting is an assessment that health insurance providers perform on people who want to get health coverage.

Companies collect information about your medical history and use it to decide:

Whether they can accept you into their program.

How much money you will pay each month for coverage.

How long you might have to wait before the plan starts to cover a specific medical condition (up to six months).

During your Open Enrollment Period, Medicare Supplement Insurance companies cannot perform medical underwriting. This means you won’t be denied coverage or have to pay higher premiums because of chronic conditions or your medical history.

When Does the Open Enrollment Period (OEP) Begin?

Most people who are eligible for Medicare get one six-month Open Enrollment Period when they turn 65 and join Medicare Part B.

This window begins on the first day of the month that your Medicare Part B (Medical Insurance) is effective.

Once your Part B coverage begins, your OEP will last for six months. During this time health insurance companies cannot use your medical history to charge you more, deny you coverage, or make you wait for coverage.

For example, if you enroll for Part B and your coverage starts on August 15th, your Open Enrollment Period will begin on August 1st and last until the end of January.

Don’t get your Open Enrollment Period mixed up with your Initial Enrollment Period. Take a look at this table to see how they’re different:

Open Enrollment Period vs Initial Enrollment Period

| Initial Enrollment Period | Open Enrollment Period | |

|---|---|---|

| What is it for? | Joining Original Medicare (Part A and B). | Joining a Medicare Supplement Plan. |

| When does it start? | 3 months before your 65th birthday month. | The first day of the month that your Part B cover begins. |

| How long does it last? | 7 months. | 6 months. |

The OEP is one of many enrollment periods that apply to Medicare. Here are some other important ones that you should know about:

| Enrollment Period | Description |

|---|---|

| Open Enrollment Period | This six-month period begins on the first day of the month when you are 65 or older and enrolled in Medicare Part B. This date will be different for everyone and depends on the month that you sign up. |

| Fall Medicare Open Enrollment Period | During this window, you can change your Medicare Supplement Insurance Plan without losing any medical coverage. This window takes place every year from October 15th to December 7th. |

| Initial Enrollment Period (IEP) | This is your first chance to sign up for Medicare once you are eligible and begins three months before your 65th birthday. During the IEP you can sign up for Medicare Parts A and B, a Medicare Advantage Plan or a Part D Prescription Drug Plan. |

| General Enrollment Period | From January 1st to March 31st you can sign up for Medicare Parts A and B, as well as a Medicare Advantage Plan if you missed the deadline. |

| Special Enrollment Period | This period refers to specific situations where you can enroll outside the regular enrollment periods (for example, if you move states or if your healthcare coverage under an employer ends). The dates for the Special Enrollment Period differ from person to person. |

If you want to learn more about these periods, read our guide to Medicare Open Enrollment Period 2022.

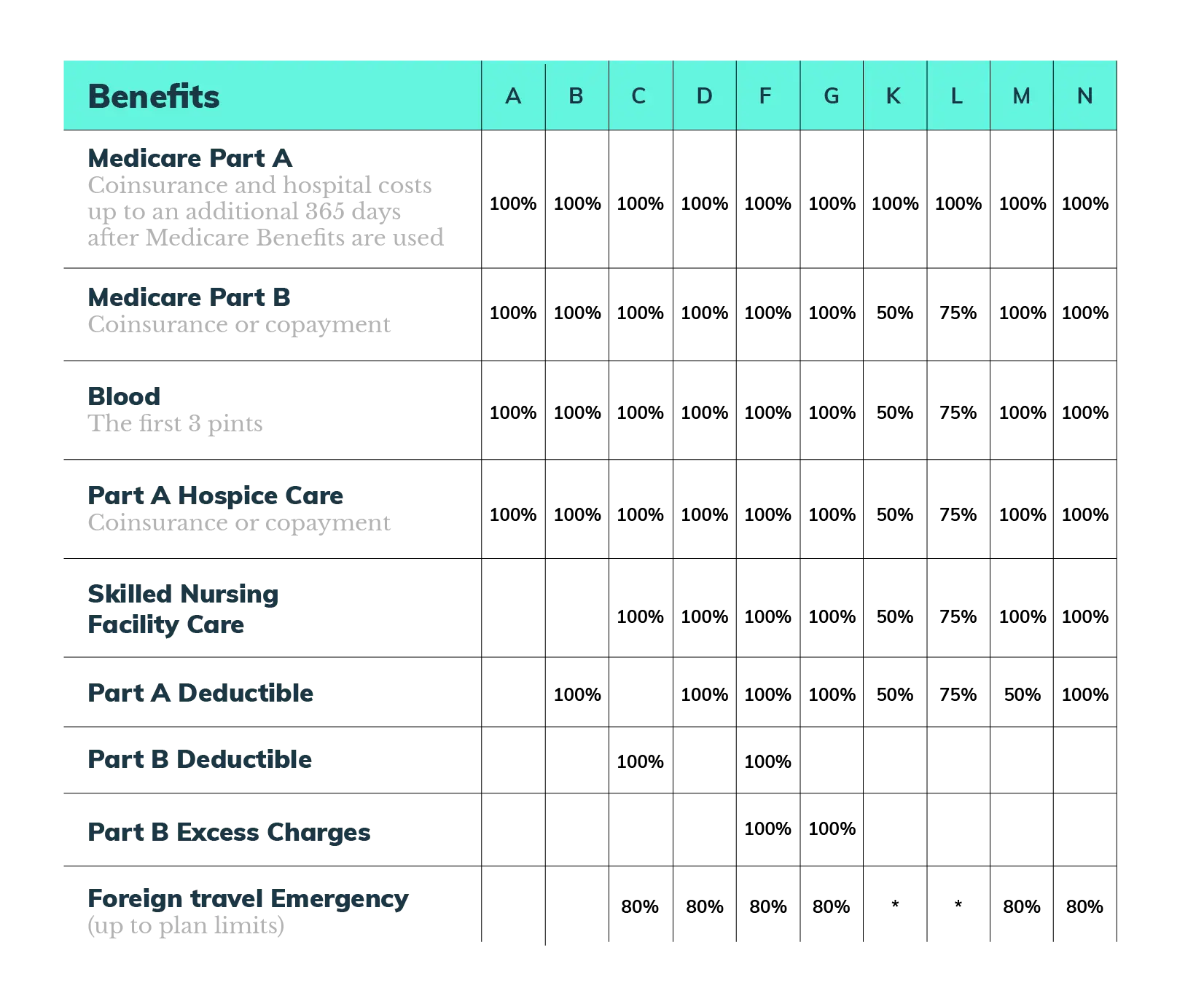

What Are the Most Popular Medicare Supplement Plans?

There are ten different Medicare Supplement Insurance Plans that you can choose from. They can be identified by a letter: A, B, C, D, F, G, K, L, M and N. The table below summarizes the essential benefits that each plan covers.

Where you see a percentage, the Medicare Supplement Plan covers that percentage of the benefit and you must pay the rest.

For example, 50% means that your plan will cover half of the treatment, service, or item costs.

Here are some other things you should know about Medicare Supplement Plans:

Plans F and G have a high-deductible option in some states. This means that if you choose one of these plans, you must pay a deductible fee of $2,370 before your insurance pays anything.

Plans K and L have out-of-pocket limits of $6,220 and $3,110. Once you have paid these amounts and the Part B deductible of $233, the plan will pay 100% of your covered services for the rest of the year.

Plans C and F will not be available to newly eligible people for Supplement Insurance on or after 1 January 2020.

Plan N will pay 100% of the Part B coinsurance. You will have to pay up to $20 for doctor visits and $50 to go to the emergency room (as long as you are not admitted to the hospital).

Let’s Take a Look at the Most Popular Plans in Ohio

Out of the 12 Medicare Supplement Insurance Plans available in Ohio, research shows that Plans F, G and N were the most popular in 2019.

Medicare Supplement Plan Enrollment Numbers (2019)

Plan F: 251,584

Plan G: 183,699

Plan N: 98,460

Medicare Supplement Insurance Plan F

Plan F is popular in many states because it offers extensive coverage for most Medicare-related costs.

There are two versions of Plan F: a standard plan and a high-deductible plan. Plan F premiums are generally more expensive than the other Supplement Plans because of the coverage they provide.

If you choose the high-deductible version, you will need to pay a $2,370 deductible fee before your plan starts to cover your health care costs.

The standard and high-deductible versions of Plan F are only available to people who became eligible for Medicare before January 1st 2020.

This means that if your 65th birthday was before 2020, you might be able to purchase this plan if it’s offered in your state.

If you’d like to find out more about the eligibility requirements of Medicare Supplement Plan F and how much it could cost you, read this article.

Plan G is another popular choice in Ohio. Like Plan F, it also has a high-deductible option that has lower premiums but a high one-off fee for coverage ($2,370).

This plan covers Part A and B deductibles, 100% of hospice care coinsurance costs, Part B excess charges, and foreign travel emergencies. However, it does not cover the Medicare Part B deductible ($233 in 2022).

This means you would have to pay your Part B annual deductible before Medicare and Plan G covers your medical costs.

For more information on Medicare Plan G coverage, costs, and benefits, take a look at this article.

Remember:

Medicare Part B covers outpatient services like specialist consultations, vaccines, screenings and walkers.

A deductible is a set amount you cover for health care before your insurance begins to pay.

Another popular Medicare Supplement Plan in Ohio is Plan N.

This plan covers most Medicare benefits, except the Part B deductibles and Part B excess charges.

Excess charges are costs that are above the Medicare-approved amounts for services, tests, and items.

For example, if you have Plan N and visit a specialist who charges higher rates than the Medicare-approved amount, you will have to pay the excess charges for their services.

Remember, because the Part B deductible is not covered you would have to pay the $233 deductible before Medicare and Plan N pays for outpatient services.

Our article on Medicare Plan N outlines everything you need to know about this Supplement Plan. This includes what it covers, how to enroll and more information about what you can expect to pay.

If you are still unsure or have any questions about Medicare Supplement Insurance plans in Ohio, contact a Medicare insurance agent at PolicyScout.

How Much Do Medicare Supplement Plans Cost in Ohio?

Although the benefits of supplemental coverage are standardized across most states, pricing can vary based on a person’s location, age, and lifestyle habits.

For example, a health insurance company may:

Want to primarily provide supplemental insurance to non-smokers.

Only offer supplement insurance in specific areas.

Charge higher premiums based on the cost of care in your state.

In general, there are three ways that an insurance company can set their premiums.

These are:

Issue-age rated: This premium will be based on the age you are when you buy the policy. Therefore, the premium is lower for people who buy it at a younger age and won’t change as you get older.

Community-rated: This premium is not based on your age. This means that the same monthly premium is charged to everyone. However, the price will vary according to inflation.

Attained-age rated: This premium is based on your current age and will increase as you get older. Although these premiums might be the least expensive at first, they will eventually become the most costly and affected by inflation.

Let’s look at an example to give you an idea of how much Medicare Supplement Insurance Plans could cost in Ohio.

Meet Greg

Greg is a 69-year-old man living in Cincinnati, Ohio. His postal code is 45207, and he is a non-tobacco user. He is trying to decide between Plans A, D and K. This is what Greg can expect to pay:

Pricing Disclaimer:

All prices and costs in this article are estimates and subject to change. They should not be viewed as the amount you will pay for Medicare Supplement Insurance.

If you want to know how much supplemental insurance might cost you, contact PolicyScout to get an accurate estimate.

(Source: Pexels)

Plan A

Plan A is a basic Medicare Supplement Plan that covers extended hospital stays or inpatient treatment.

In Ohio, monthly premiums for Plan A range between $83 and $429 for Greg. This amount does not include the $170.10 standard monthly premium for Medicare Part B.

Example - Greg’s Monthly Expenses for Plan A

Plan A Monthly Premium: $83 - $429

Medicare Part B Premium: $170.10

Total Monthly Costs: $253.10 - $599.10

On Plan A, he will still have to pay Part A and B deductibles and coinsurance amounts. He will not be covered for Part B excess charges and doesn’t get insurance for foreign travel emergencies.

If Greg ever needed care in a skilled nursing facility, his Plan A insurance would not cover these expenses.

However, if he is hospitalized for longer than 90 days, his Medicare Supplement Plan will pay his hospital expenses for a maximum of 365 days after his Original Medicare cover ends.

Here’s a comparison of what it would cost if Greg is hospitalized for 150 days because of a life-threatening illness:

Hospitalization for 150 Days: Original Medicare vs Plan A

| Original Medicare Only | Original Medicare with Plan A coverage |

|---|---|

| Part A Deductible (2022): $1,556 | Part A Deductible (2022): $1,556 |

| Day 1-60: $0.00 | Day 1-60: $0.00 |

| Day 61-90: $389 per day ($11,670) | Day 61-90: $0.00 |

| Day 91-150: $778 per day ($46,680) | Day 91-150: $0.00 |

| Total Costs: $59,906 | Total Costs: $1,556 |

Plan A Benefits:

❌ Skilled Nursing Facility

❌ Part A Deductible

❌ Part B Deductible

❌ Part B Excess Charges

❌ Foreign Travel Emergency

A Recap of Key Terms:

Deductible: This refers to the set amount you pay for health care services before your insurance begins to pay.

Coinsurance: The percentage of costs you pay after your deductible has been paid.

Copayment: A set rate you must pay for doctor visits, hospital stays and prescriptions.

Plan D

For Greg, Medicare Plan D premiums range between $130 to $317

Example - Greg’s Monthly Expenses for Plan D

Plan D Monthly Premium: $130 - $317

Medicare Part B Premium: $170.10

Total Monthly Costs: $300.10 - $487.10

He will not have any copayments or coinsurance for Part A and Part B costs, but he will have to meet the $233 Medicare Part B deductible before his insurance starts to cover his costs.

If he is hospitalized, he will not have to pay the Part A deductible ($1556 in 2022), but he will have to cover the Part B excess charges.

He will have foreign emergency travel benefits (maximum lifetime benefit of $50,000). However, he will have to pay a $250 deductible before he can get these benefits.

Plan D Benefits:

✅ Skilled Nursing Facility

✅ Part A Deductible

❌ Part B Deductible

❌ Part B Excess Charges

✅ Foreign Travel Emergency

Plan K

If Greg chooses Medicare Supplement Plan K, he can expect to pay between $47 to $140 every month. He will have to pay this amount on top of his Medicare Part B monthly premium.

Example - Greg’s Monthly Expenses for Plan K

Plan K Premium: $47 - $140

Medicare Part B Premium: $170.10

Total Monthly Costs: $217.10 - $310.10

On Plan K, Greg will get 10% of his Medicare Part B expenses covered until they reach $6,220 (maximum cost plan limit). After this, Plan K will cover all of his Part B expenses for the year.

Plan K will pay half of Greg’s Part A deductible ($1556) if he is hospitalized, and he will have to pay the full $233 Medicare Part B deductible.

He can expect to pay excess charges for visits to doctors who don’t accept Medicare and he won’t get foreign travel emergency benefits.

Plan N Benefits:

✅ Skilled Nursing Facility

✅ Part A Deductible

❌ Part B Deductible

❌ Part B Excess Charges

❌Foreign Travel Emergency

The table below summarizes the costs and benefits of each Medicare Supplement Plan Greg is interested in:

| Plan A | Plan D | Plan K | |

|---|---|---|---|

| Monthly premiums | $83 to $429 | $130 to $317 | $47 - $140 |

| Medicare Part B premium cover | No | No | No |

| Copayments | None for approved Part B (outpatient) services. | None for approved Part B (outpatient) services. | N/A |

| Deductible costs | $233 (Part B) $1556 (Part A) | $233 (Part B) | $233 (Part B)Half of the Part A deductible ($778) |

| Foreign Travel Emergency Cover | No | Yes | No |

| Part B Excess Charges | Not covered | Not covered | Not covered |

As you can see, Medicare Supplement plans have different costs, benefits, and coverage options.

The great thing about this is that you can find a plan that suits your individual medical needs, but it's difficult to read the fine print and decide which plan is right for you.

If you need assistance, you can visit Medicare.gov or the Centers for Medicare and Medicaid Services (CMS) website if you want to find out what a plan might cost.

You can also reach out to a licensed insurance agent if you want to find a provider or learn about the different Medicare plans available.

Where Can I Find Out More about Medicare and Supplement Insurance?

Learning about Medicare can save you money, time, and hassles in the long run. If you’re interested in finding out about Medicare or Medicare Supplement Insurance plans, our Medicare Hub is a good place to start.

We also have a team of experienced Medicare consultants who can help with your questions over the phone or in writing.

If you’d like to speak with an insurance agent about your Medicare insurance options, call us on 1-888-912-2132 or email us at Help@PolicyScout.com.