State Farm Life Insurance 2022 Review

Read our review on State Farm Life Insurance and find out how it compares with other life insurance companies. Being well informed helps you make the right decisions when choosing life insurance.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

Do I Need Life Insurance?

Have you heard of family or friends in financial difficulty after the breadwinner passes away?

The simple solution to protecting the financial future of your family is to take out life insurance.

A payout from a life insurance policy can be used in different ways:

To pay death taxes so that assets do not need to be sold to pay these taxes.

To leave a cash legacy to family members.

To pay the bills when a breadwinner dies.

To settle a student loan, vehicle loan, or mortgage.

How Much Life Cover Do I Need?

The answer to this question will vary between individuals.

Think about how much money would be needed by your family if your income is no longer available for household expenses; how your children will pay their student loans; and whether you still have to repay your mortgage once you reach retirement age.

Factors such as your age, financial situation, the family’s income, and outstanding debt will determine how much life insurance cover you need.

The Cost of Life Insurance

A life insurance policy is a contract between you and a life insurance company to pay a sum of money to your beneficiaries at your death.

To calculate the price, or premium, the insurer has to assess the chances of you dying and when this is likely to happen.

The shorter your life expectancy, the more you can expect to pay for life insurance.

The following factors play a role in what life insurance will cost you:

Age

Unless caused by accident, older people tend to die sooner than younger people.

Gender

Women tend to live longer than men and will pay less for cover than men.

Occupation

An office job is less risky than working on an oil rig. The higher the risk, the higher the premiums will be.

Lifestyle

Dangerous hobbies such as scuba diving or rock climbing will drive up your policy’s premium.

Driving record

Speeding, frequent accidents, or DUIs on your record will impact policy premiums.

Smoking status

Smoking leads to a shorter life and it’s an important factor that life insurers take into account. Smokers will pay more for life cover than nonsmokers.

Family health history

If your family has a history of heart disease or cancer, your premiums will be higher because your chances of developing such illnesses is higher than for other people.

The type of policy, coverage amount, and life insurer you choose will also have an impact on the policy premium.

Terms you need to know -

Life insurance companies include exclusions, limitations, possible reductions in benefits, and other conditions in their policy contracts. Make sure you understand the details.

About State Farm Life Insurance

State Farm has been around since 1922 and today it’s one of the top 10 largest life insurance companies in the country, based on the combined value of premiums.

State Farm Life Insurance Company (not licensed in MA, NY or WI) and State Farm Life and Accident Assurance Company (licensed in NY and WI) are the two business units that provide life insurance in the U.S.

Pros and Cons of State Farm Life Insurance

✅ Financially strong insurer.

✅ Highly ranked for consumer satisfaction.

✅ Wide range of policies.

✅ Many optional riders that offer additional benefits.

✅ Offers instant answer life policies which do not require a medical exam.

✅ Digital tools include a mobile app and online tools to manage policies.

❌ Term life premiums may not be competitive.

❌ Not all policies are available in every state.

❌ Low level of cover for instant answer policies.

❌ Age restrictions on some policies.

Life Cover Offered by State Farm Life Insurance

State Farm offers a range of term life, whole life, and universal life policies available in all states except Massachusetts and Rhode Island.

Term life cover

Of the three types of life insurance, term life insurance is the simplest form of life cover. Initially it is also the cheapest life cover.

With term life insurance, you sign a contract for a fixed term with a life insurance company, and pay a monthly premium in return for the insurer paying out a sum of money at your death.

After the term has expired, you may be able to renew the policy or convert it to a permanent life insurance policy.

The term of the policy is typically 10, 15, 20, or 30 years and the cash benefit can be paid out to anybody you choose to receive it. The recipient of the benefit is called a beneficiary.

If you choose the same monthly premium for the full term of the policy, it is called a level premium policy.

Term Life Insurance from State Farm

Source: Forbes.com

Permanent life insurance

Also called whole life cover, this type of policy is used when you need lifelong life insurance cover. Provided you pay the premiums, it remains in place regardless of how old you get.

It differs from term life policies in that whole life cover has a death benefit as well as a savings benefit.

The savings benefit is from dividends that the insurer allocates from time to time, which also earn interest free of tax.

The advantage of a policy with a savings or cash benefit is that you can withdraw the cash from the policy, or borrow money from the insurer from the cash portion.

As the policyholder, you can access the cash value, but your beneficiaries will receive only the death benefit, not the cash portion.

There are implications to either withdrawing or borrowing from the cash portion of your policy. You will pay interest on any loans and, if you make any withdrawals, the death benefit may be reduced. This means less money will be available to your beneficiaries.

State Farm offers the following whole life insurance:

The standard option is a whole life policy with premiums that stay the same.

Single-premium policies allow you to prepay the policy with one up-front payment.

Limited-pay policies allow you to pay premiums over a set number of years—between 10 and 20 years. After that the cover remains in place, but you don’t need to pay premiums.

Final expense life insurance, which provides cover for deathbed and funeral expenses. It offers coverage of $10,000 and is available to applicants between 50 and 80 years—except in New York, where the cutoff age is 75 years.

Remember -

The benefit of prepayment is that you do not have to pay policy premiums, for instance, at retirement age when your income may start decreasing.

Universal life cover

With universal life insurance policies, you have some flexibility to raise and lower premiums, and to adjust the death benefit amount.

As with whole life cover, it remains in force for the duration of your life and it has a cash value benefit. Universal life insurance generally costs less than whole life insurance.

As with whole life policies, the interest earned on the savings portion of the policy does not incur tax.

The downside of a universal life policy is that the cash value can be eroded, or even wiped out, by the insurer’s monthly expenses and costs that are charged to your policy.

State Farm allows anybody up to the age of 85 to buy universal life insurance and offers them two options:

Survivorship universal life cover

This cover lasts until the death of a spouse, after which the death benefit is paid out to the beneficiaries. These policies are useful for paying estate taxes, and leaving funds in a trust for children with special needs.

Joint universal life cover

Covers both spouses under a single plan, but pays out after the first person dies. The death benefit payout can serve to take care of the monthly living expenses of the remaining spouse.

Other forms of universal life cover from life insurance companies are variable universal life cover and indexed universal life insurance. The difference between these types and traditional universal life insurance is how the cash portion of the policy can be invested to earn growth.

State Farm Life Insurance only offers traditional universal life insurance policies.

The Benefits Offered by Policy Riders

Insurance riders are further benefits that can be added to an insurance contract. Riders can be added to a policy when you first take it out, during the term of a policy or when it comes up for renewal.

You can choose which riders to add to your policy, provided they are offered by the life insurance company on the type of policy you are buying. Riders cost extra as they offer additional benefits.

Here are some of the riders available from State Farm Life Insurance:

Waiver of premium

This is one of the most common riders. It allows you to stop paying premiums, without losing cover, if you become disabled and unable to perform your job. Waiting periods may apply before benefits start.

Flexible care benefit rider

A flexible care benefit rider allows you to access a portion of the policy’s death benefit every month should you become impaired due to a chronic disease.

Select term rider

A select term rider gives you peace of mind that your policy cover will remain in place up to the age of 95, and that the premium will not increase over the term you choose. The term can be 10, 20, or 30 years.

Guaranteed insurability rider

This option allows you to increase your cover at specific option dates and still pay the standard rate. This rider is available without a medical exam, if you’re between the ages of 17 and 49.

Level term rider

Such a rider gives you the option of buying additional coverage until the age of 95.

Level term rider for an additional insured person

With this rider, the premium remains at the same level for your spouse or any other person on your policy for the amount of the rider until the age of 95.

Waiver of monthly deduction for death or disability

The benefit under this rider is that you will not have to pay monthly premiums should you become totally disabled for six months or more prior to the age of 60.

Future premiums are also waived should you die prior to turning 65. This is something that you may need for a joint life insurance policy.

Estate preservation rider

The benefit of this rider is that you get an additional death benefit to help offset estate taxes should you die within the first four years of taking out the policy.

Some riders may be restricted to certain policies and to certain states.

State Farm Life Insurance Review and Ratings

| State Farm Life Insurance | Northwestern Mutual Life | New York Life | Prudential | |

|---|---|---|---|---|

| Customer Satisfaction Rating ConsumerAffairs Rating (out of 5 stars) | 4 stars | 3.8 stars | 3.8 stars | 3.4 stars |

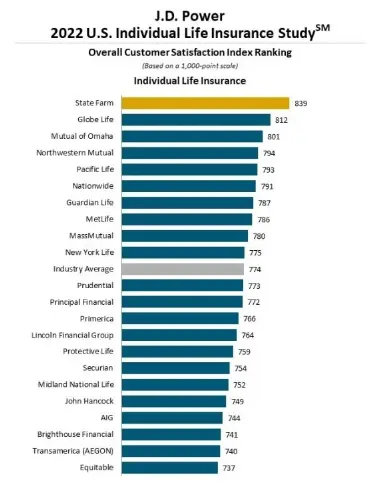

| Customer Satisfaction Rating 2022 J.D. Power Study Ranking, industry average ranking is 776. | 839 out of 1,000 | 794 out of 1,000 | 775 out of 1,000 | 773 out of 1,000 |

| Financial Strength Rating AM Best (financial strength rating range is D to AA++) | A++ (superior) | A++ (superior) | A++ (superior) | A+ (superior) |

| Complaint Rating 2021 NAIC Rating Note: Ratings below the median of 1 show the insurers have fewer complaints than the national median. Ratings above 1 indicate more complaints than the median. | 0.12 for State Farm Life and Accident Insurance Company 0.20 for State Farm Life Assurance Company | 0.03 | 0.35 for New York Life Group Insurance Company 0.03 for New York Life Insurance and Annuity Corporation 0.17 for New York Life Insurance Company | 0.67 for Prudential Insurance Company of America |

| Insurance Policy Products | Term life Whole life Universal life | Term life Whole life Universal life Variable universal life Whole life | Term life Whole life Variable universal life | Term life Indexed universal life Indexed variable universal life Variable universal life |

Guide to Buying Life Insurance Cover

Decide on the type of insurance, the amount of cover, the riders you want, and then shop around.

It is worth comparing prices for a policy, but always compare apples with apples.

Also, don’t base your buying decision solely on price. Other factors to consider include: customer service standards, financial stability, how easy it is to claim, and the insurer's reputation for paying claims quickly.

You can apply for a term life insurance quote online at State Farm Life Insurance, but if you need permanent life cover you need to contact a State Farm agent.

What Life Insurance Does Not Cover

Your policy will pay out the coverage amount in the contract, but all policies have conditions and exclusions. For example, preexisting conditions, suicide (typically in the first two years of the policy), and driving under the influence of alcohol or drugs may be reasons for an insurer to refuse paying out your claim.

Summary: Why Buy Life Cover from State Farm Life Insurance

State Farm Life Insurance is an established, financially strong business with excellent rankings for customer satisfaction. Our State Farm Life Insurance review shows that the company is worth considering for your life insurance needs.

Evidence of its financial strength is an AA++ rating from ratings agency AM Best. This means its finances are rated as “superior”.

According to the consumer research and data analytics company J.D. Power, State Farm is the top ranked individual life insurer for customer satisfaction for the third year running.

Source: 2022 U.S. Individual Life Insurance Study

State Farm’s insurance companies also achieved excellent ratings for their low level of customer complaints from the National Association of Insurance Commissioners (NAIC)

The NAIC measures complaints from customers on an index from 0 to two. An index rating of 0 means no complaints were received, while a rating of 2 means the life insurance company received double the number of complaints compared to the median insurer.

Both State Farm Life and Accident Insurance Company and State Farm Life Insurance Company received very favorable ratings of 0.12 and 0.20, indicating very low numbers of complaints.

Another third party, ConsumerAffairs, awarded State Farm 4 out of 5 stars based on actual customer reviews. Since this is an average, some reviewers awarded the insurer only one or two stars, but most gave it between 3 and 5 stars.

State Farm Life Insurance is worth considering if you are looking for term-, whole-, or universal life insurance cover. Its policies have flexible premiums, coverage amounts, and a wide range of useful riders to add to your policy for further benefits.

If you are looking for instant answer life insurance—which does not require a medical exam—State Farm’s options are limited, so other life insurers may be better for your needs.

Some third parties, such as the magazine Money, report that State Farm’s life products may be more expensive than those from other insurers, but price should not be the sole driver of your decision-making.

Frequently Asked Questions (FAQs)

Is State Farm Life good at paying claims?

State Farm has an excellent reputation for its service levels, but the experience of individual customers varies.

How much money can I borrow from a State Farm life policy?

The type of policy determines whether there is a cash benefit from which you can borrow, and the maximum you can borrow is based on the cash value that has built up in your policy. The longer it has been in force, the higher the cash value is likely to be.

How do I submit a life insurance claim on a State Farm policy?

You can submit a claim in two ways: by calling a State Farm agent in your state or online at the online claim center.

Need More Information? Contact PolicyScout for Life Insurance Advice!

You can reach us at 1-888-912-2132 or send an email to Help@PolicyScout.com to get assistance from one of our trained consultants about your options.