John Hancock Life Insurance 2022 Review

Read our 2022 review on the pros and cons of John Hancock Life Insurance, the policies it offers, and its reputation in the market. You can choose the right life insurance policy when you have the facts.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

What Is Life Insurance?

A life insurance policy is a contract between you and a life insurance company to pay a sum of money to your beneficiaries when you pass away. The money paid is called a death benefit.

You can nominate one or more people to receive the death benefit and you can choose what percentage of the payout each should receive.

Your beneficiaries will need to file a claim with the relevant life insurance company to receive the death benefit.

Remember -

If you do not name beneficiaries to receive the death benefit, the money will be paid into your estate and it will be tied up in a lengthy estate probate process.

Probate is the legal process of settling debts and dividing assets among heirs.

Do I Need Life Insurance?

If you have people in your life who depend on you financially, you need life insurance.

Life insurance protects the financial future of your family by providing a replacement income so they can pay bills and other expenses when you are no longer around.

Life insurance serves other purposes, too. Here are some examples of just how useful life insurance can be:

To provide cash in an estate for death taxes so that assets do not need to be sold.

To leave a cash legacy to family members.

To pay for college loans, car loans, health care expenses, or an outstanding mortgage.

How Much Life Cover Do I Need?

The starting point is to consider how much money your family will need if your income is no longer available to cover household expenses, debt repayments, and other financial commitments.

Also think about whether you have sufficient cash savings for the payment of death taxes and any estate taxes.

Factors such as your age, financial situation, the family’s income, and outstanding debts will determine how much life insurance cover you need.

The Cost of Life Insurance

The cost of a life insurance policy is determined by a number of factors, such as your age and health, as well as the amount and duration of cover.

The following factors play a role in what life insurance will cost you:

Age

Unless caused by an accident, young people will live longer than older people. The shorter your life expectancy, the more you can expect to pay in premiums.

Gender

Women tend to live longer than men and will pay less for cover than men.

Occupation

An office job is less risky than working on an oil rig. The higher the risk, the higher the premiums will be.

Lifestyle

Dangerous hobbies such as scuba diving or rock climbing will drive up your policy premium.

Driving record

Speeding, frequent accidents, or DUIs on your record will impact policy premiums.

Smoking status

Smoking leads to premature death and it’s a key factor that life insurers take into account. Smokers will pay more for life cover than nonsmokers.

Family health history

If your family has a history of heart disease or cancer, your premiums will be higher because your chances of developing such illnesses are higher than for other people.

The type of policy, coverage amount, and life insurer you choose will also have an impact on the policy premium.

Remember -

Life insurance companies include exclusions, limitations, possible reductions in benefits, and other conditions in their policy contracts. Make sure you understand the details.

About John Hancock Life Insurance

John Hancock has been around for 160 years and is one of the largest life insurers in the U.S.

It operates as a division of the international financial services business Manulife Financial Corporation after it was taken over by Manulife in 2004.

Life Cover Offered by John Hancock

Johan Hancock offers a range of term life and permanent life insurance policies.

Term life cover

Term life cover lasts for a set amount of time and John Hancock gives you term options of 10, 15, 20, or 30 years with cover of between $250,000 and $65 million. It is available to anybody between the ages of 18 and 80 years.

Term life cover is cheaper than permanent life insurance and you pay the same premium for the duration of the chosen term of policy. Some insurers allow you to extend the policy by adding additional terms, but then premiums will increase.

If you live longer than the selected term of your policy, your policy ends and no benefits are payable.

Your beneficiaries will receive a payout only if you die during the term of the policy, so make sure that this type of insurance is suitable for you.

John Hancock’s term life insurance has an option to convert your term policy to a permanent policy.

Permanent life insurance

Permanent life cover policies remain in place regardless of how old you get, provided you keep paying the premiums.

There are two broad types of permanent life insurance in the insurance market: whole life policies and universal life policies.

Unlike term life insurance, whole life insurance and universal life insurance both have a death benefit as well as a cash value benefit.

The cash portion can be withdrawn or borrowed against by the policyholder. But, your beneficiaries do not have access to the cash portion; they will only receive the death benefit portion.

There are implications to borrowing or withdrawing cash from your policy. You will pay interest on any loans and, if you make any withdrawals, the death benefit may be reduced. This means less money will be available to your beneficiaries.

The interest, dividends, or capital gains on the cash portion of the policy are not taxed, unless you withdraw the cash.

Universal Life Insurance

Universal life insurance generally costs less than whole life insurance, and it offers the flexibility to adjust the amount and frequency of the premiums. With a whole life policy, your premiums and the death benefit remain the same throughout.

On the downside, the cash value of a universal life policy can be eroded or even wiped out by the insurer’s monthly expenses and costs that are charged to your policy.

John Hancock’s universal life insurance policies are available to anybody from three months to 90 years of age, with coverage amounts ranging between $50,000 and $65 million.

The difference between the types of universal life policies from John Hancock is how the cash value of the policy earns growth. Here are the options:

- Traditional universal life

The life insurer allocates interest to the cash portion from time to time. The rate is set by the life insurer and can vary.

- Variable universal life

You can choose to invest the cash portion in a range of sub investment accounts with varying degrees of risk. While this type of policy has the best potential for growth of the cash portion, it also carries the most risk. If you don’t pick investments that will deliver returns, you can lose investment growth.

- Indexed universal life

The cash value in an indexed universal life policy earns growth from the performance of a stock market index, such as the S&P 500. An index is a basket of shares that represent a market sector or index. It allows investors to gain exposure to a market sector without having to purchase all the shares in that sector.

Remember -

You can adjust the premiums on a universal life policy. If you decrease your premium, make sure there is enough money to cover the policy costs. If not, the policy could lapse, leaving you with no life cover.

Be aware that policy costs increase as you get older.

Pros and Cons of John Hancock Life Insurance

✅ Competitive rates for seniors on term life cover.

✅ Term life insurance which does not require any medical exam is available for some people.

✅ Discounted premiums are offered on its healthy lifestyle program.

✅ Has life cover specifically for diabetics.

❌ Customer service levels are mediocre.

❌ Does not offer whole life insurance.

The Benefits Offered by Policy Riders

Insurance riders offer a way to customize an insurance policy. They are added onto an insurance contract to extend coverage, or add other benefits.

Some riders have become commonplace and are offered on insurance policies as a matter of course, but others must be purchased.

The added benefits will cost more but it may be worth it if it covers a specific need. You can add a rider when you first take out a policy, during the term of the policy, or at the renewal stage.

The riders you can choose will depend on what is available from the insurance company, the state where you live, and your specific policy type.

Here are some of the riders available from John Hancock Life Insurance:

Accelerated benefit rider

Should you be diagnosed with a terminal disease, this rider will allow you to access the death benefit early to assist you with paying medical costs. The percentage of the benefit you are allowed to take will depend on the terms of the policy rider.

Disability benefit rider

If, prior to the age of 65, you are disabled for six months, or more, and unable to do your job, you can access some of the death benefit of the policy.

The benefit may be a set monthly amount, a percentage of the death benefit, or a percentage of the premium.

Critical illness benefit rider

If you fall ill with a critical illness such as cancer, a portion of the death benefit is paid out as a lump sum.

Long-term care rider

You can claim benefits under this rider if you are unable to perform certain daily living activities, or suffer impairment of cognitive functions due to a chronic illness or condition.

You need to meet very specific criteria to qualify for benefits. The criteria will be set out in your policy contract.

John Hancock Vitality Rewards Program

The insurer’s optional Vitality Rewards Program is available on both term or permanent life policies.

Under the program you earn Vitality Rewards for making healthy lifestyle choices such as buying healthy foods, exercising, and even for meditating to keep your mind healthy.

The rewards include discounts on your premium, as well as savings on fitness devices, groceries, travel, and retail goods.

John Hancock Aspire with Vitality Program

The Aspire Program is an optional benefit specifically for policyholders who have type 1 or type 2 diabetes. It provides incentives to diabetics who take steps to manage their health, and rewards them with discounted premiums, as well as discounts on groceries, travel, and retail items.

In addition, diabetics on the Aspire with Vitality Program are supported on their wellness journey by virtual consultations with medical experts, personalized health coaching, and free diabetes testing devices.

John Hancock Life Insurance Review and Ratings

| John Hancock | Northwestern Mutual Life | State Farm Life Insurance | Prudential | |

|---|---|---|---|---|

| Customer Satisfaction Rating ConsumerAffairs Rating (out of 5 stars). | 3.8 stars | 3.8 stars | 4 stars | 3.4 stars |

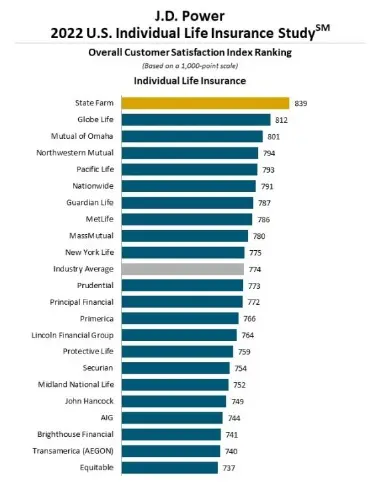

| Customer Satisfaction Rating 2022 J.D. Power Study Ranking, industry average ranking is 776. | 749 out of 1,000 | 794 out of 1,000 | 839 out of 1,000 | 773 out of 1,000 |

| Financial Strength Rating AM Best (financial strength rating range is D to AA++). | A+ (superior) | A++ (superior) | A++ (superior) | A+ (superior) |

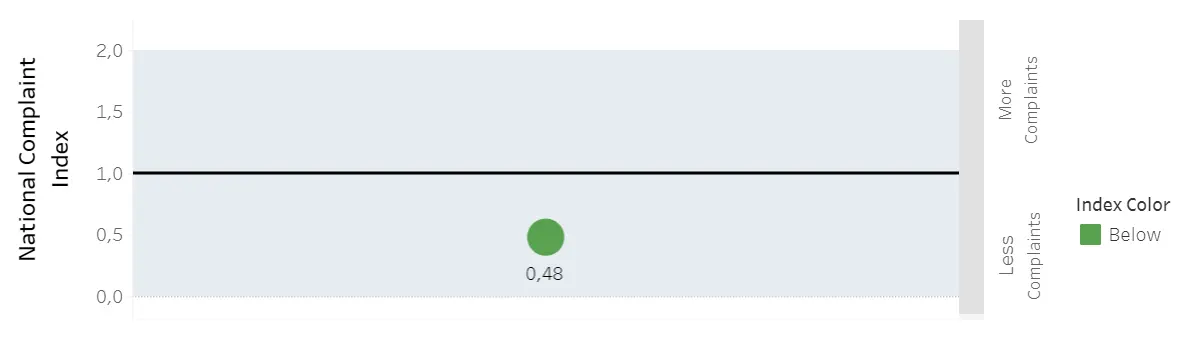

| Complaint Rating 2021 NAIC Rating Note: Ratings below the median of 1 show the insurers have fewer complaints than the national median. Ratings above 1 indicate more complaints than the median. | 0.48 for John Hancock Life Insurance Company of NY; 0.34 for John Hancock Life Insurance Company USA | 0.03 | 0.12 for State Farm Life and Accident Insurance Company; 0.20 for State Farm Life Insurance Company | 0.67 for Prudential Insurance Company of America |

| Insurance Policy Products | Term life Universal life Variable universal life Indexed universal life | Term life Whole life Universal life Variable universal life Whole life | Term life Whole life Universal life | Term life Indexed universal life Indexed variable universal life Variable universal life |

Guide to Buying Life Insurance Cover

Decide on the type of insurance, the amount of cover, the riders you need, and then shop around. Compare like with like and, if your knowledge of life insurance is limited, get expert advice.

Don’t base your buying decision solely on price—customer service standards, financial stability, how easy it is to claim, and the insurer's reputation for paying claims quickly all count.

To get a life cover quote from John Hancock, call 888-955-5432 to talk to an advisor, or fill in the contact request form for the insurer to get in touch with you.

What Life Insurance Does Not Cover

Your policy will pay out the coverage amount in the contract, but all policies have conditions and exclusions. Examples are preexisting conditions, suicide (typically in the first two years of the policy), and driving under the influence of alcohol or drugs may be reasons for an insurer refusing to pay out a claim.

Summary: Why Buy Life Insurance from John Hancock

John Hancock Life Insurance Company is a good choice for its healthy lifestyle incentive program which offers discounted premiums, gym memberships, and other benefits.

Its rates for those in their fifties and sixties are competitive, but for younger age groups, it can be expensive.

The insurer prides itself on having life cover for diabetics and on its website, claims to be the only insurance company offering such cover.

With an A+ rating from ratings agency AM Best, John Hancock is in a good position to pay out claims, and to honor policy guarantees and riders.

A J.D. Power study and the ConsumerAffairs website, however, show that the company struggles to deliver service in some cases.

John Hancock’s index ranking of 749 out of 1,000 in the J.D. Power’s 2022 U.S. Individual Life Insurance Study places it 18th from the top, and eight notches below the average.

Source: 2022 U.S. Individual Life Insurance Study

ConsumerAffairs gave the insurer 3.8 out of 5 stars based on reviews from 136 customers on the website.

But, the National Association of Insurance Commissioners (NAIC) found that the John Hancock Life Insurance Company of NY, and John Hancock Life Insurance Company USA, had complaint index ratios below the median number of complaints for similar companies on individual life policies. These ratings are given across all products.

John Hancock Life Insurance Company of NY

Source: NAIC

John Hancock Life Insurance Company USA

Source: NAIC

Explanation of NAIC graphs above: The NAIC measures complaints from customers on an index from 0 to two. The complaint index is always 1.00. Those companies with an index rating of below 1.00 received fewer complaints than the median. A rating of 2 means the life insurance company received twice the number of complaints compared to the median insurer.

According to the Better Business Bureau (BBB), 33 customers filed complaints against the John Hancock Life Insurance Company USA in the last 3 years, at the time of writing.

The BBB gave the company a “B” rating. The ratings scale ranges from A (the best rating) to F (the worst rating).

Their ratings reflect the BBB’s view on how well a company is likely to interact with its customers. It is based on data obtained by the BBB that includes the company’s complaints history, how long the business has been in operation, the transparency of its business practices, licensing, and government actions that the BBB learns about.

Frequently Asked Questions (FAQs)

How long does it take for a payout after a death claim is submitted?

According to John Hancock Life Insurance’s website, you can expect to receive a payout between 7 and 10 business days.

How much will my family receive from my life insurance policy?

In most cases the death benefit is the amount of cover that you chose when you bought the life policy and in some cases, any interest earned on it is added. Any loans that you took against a policy’s cash value will be deducted. The payout will be affected if you do not keep up with your premiums.

Need More Information? Contact PolicyScout for Life Insurance Advice!

You can reach us at 1-888-912-2132 or send an email to Help@PolicyScout.com to get assistance from one of our trained consultants about your options.