UnitedHealthcare Health Insurance Review

UnitedHealthcare (UHC) is the biggest health insurance provider in the U.S., with 6.5 million members nationwide.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

Although their plans are more expensive than other health insurance companies, UnitedHealthcare has very positive customer reviews and offers broad Medicare coverage.

The health insurance provider has good customer service if you look at their online reviews. And they also have a useful UnitedHealthcare app for members, which they can use to manage and monitor their health insurance plan.

While UnitedHealthcare has many extra benefit programs and telehealth options, this health insurance option is limited in terms of state availability. While they have health insurance plans in every state, certain plans are only available in some states.

Terms you need to know -

Extra benefit programs include things like fitness and wellness benefits that are included with the health insurance plan you choose.

Read our full review of UnitedHealthcare to decide if they are the right health insurance company for you.

An Introduction to UnitedHealthcare

UnitedHealthcare falls under the UnitedHealthcare Group, founded in 1974 in Minnesota.

The group includes Optimum, which is a health services information technology company, and UnitedHealthcare. Operating with a health services information technology company means UnitedHealthcare members benefit from technological advancement and innovation.

Based on its revenue, the UnitedHealthcare Group is the largest health care company in America.

There is a list released every year by Fortune magazine of the biggest companies in America. UnitedHealthcare ranks 11th on that list.

A bigger health insurance company can be both good and a bad.

UnitedHealthcare provides:

Health benefit plans and services for employees who work for businesses.

Health and wellbeing services to people who are 65 years old and older.

State programs like Medicare and Medicare Advantage Plans.

Its main goal is to offer a full range of health benefits and to simplify the health care experience for its members.

UnitedHealthcare offers Medicare Advantage Plans in all 50 states and Medicare Supplement Insurance—Medigap—nationwide.

Medicare Advantage Plans are for people who want to use government Medicare through an insurance provider.

Medicare Supplement Insurance is for people who are on Medicare but need more coverage than what Medicare provides.

The Pros and Cons of UnitedHealthcare

Before you can make a decision if UnitedHealthcare is the right choice for you, it’s a good idea to understand the pros and cons of this specific health insurance provider.

✅ Pro: Partnership with AARP

UnitedHealthcare is the only health insurance provider that has partnered with the American Association of Retired Persons (AARP), which is an interest group in the U.S. that focuses on issues affecting people over the age of 50.

The partnership has resulted in the co-branding of Medicare insurance plans which remain at the same cost as you age.

✅ Pro: The largest network of providers

Another reason that UnitedHealthcare’s high premiums may be worthwhile, is that their insurance plans cover the widest network of health care professionals.

A network of health care professionals is the group of doctors that a health insurance company will pay for.

UnitedHealthcare offers coverage for over 65,000 health care facilities and hospitals nationwide.

✅ Pro: Telehealth and home visits

From an annual house visit to extensive telehealth benefits, UnitedHealthcare offers quite a few ways for you to get health care from your home.

This is really useful if you can’t get around on your own or if you are too sick to visit a doctor’s office.

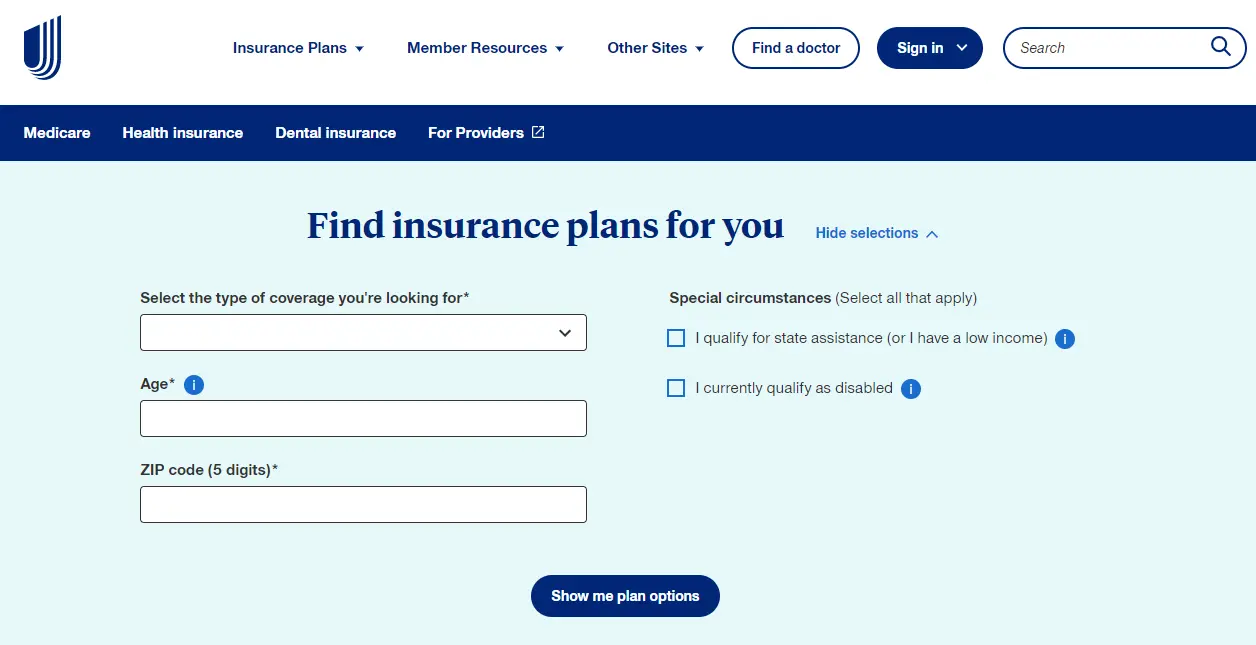

✅ Pro: Online plan recommendation tool

On their website, UHC has a useful plan recommendation tool to help you make an informed decision about which plan is best for you.

Using an online plan recommendation tool lets you be specific about what you need from a health insurance plan. It also shows you comparisons between plans so you can choose the right one for you.

Here is what their online insurance plan finder looks like:

source: uhc

Their recommendations are based on your specific needs, such as doctors, medications, and travel.

The tool will ask you several questions to find out what your circumstances are and will then recommend the right plan for you.

✅ Pro: The largest network of providers

Another reason that UnitedHealthcare’s high premiums may be worthwhile, is that their insurance plans cover the widest network of health care professionals.

A network of health care professionals is the group of doctors that a health insurance company will pay for.

The insurance company offers coverage for over 65,000 health care facilities and hospitals nationwide.

The benefits of having access to a larger network mean you have more doctors to choose from. There is also less chance of you having to pay money out of your pocket to see a health care provider.

❌ Con: A high price tag

Being the largest health insurance company in America, you might think their monthly premiums would be the same or lower than other companies. But this is not the case.

Many UnitedHealthcare Medicare Advantage Plans are actually more expensive than other health insurance companies.

Also, their plans often have higher out-of-pocket maximums than other providers.

An out-of-pocket maximum is the amount of money you need to pay for health services before your Medicare Advantage Plan starts paying.

While you may get more extra benefits for this higher price tag, you may want to consider cheaper options if you have a small budget.

❌ Con: Availability

While UnitedHealthcare operates in all U.S. states, not all its plans are available in every state. Depending on where you live, you may have a limited range of plans to choose from.

❌ Con: Customer satisfaction

In some cases, UnitedHealthcare’s customer service ratings are low. You will see more about their ratings later in this review, but some of their ratings are lower than other health insurance companies.

You would want to choose a health insurance provider that has good customer service so that you can get the help you need when you need it.

What Do UnitedHealthcare Insurance Plans Cover?

Not all health insurance plans are created equal. Some insurance providers only cover a limited number of medical expenses, while others have more coverage.

Let’s look at what UnitedHealthcare’s insurance plans cover.

Children's Health Insurance Program (CHIP)

If your child is not on a health insurance plan, the Children's Health Insurance Program gives coverage to infants, children, and teens. This is different from having your child listed as a dependent on your family health insurance.

Plans that provide coverage for dependents are required to extend the coverage of dependents to age 26, regardless of their eligibility for other insurance.

Parents can benefit from CHIP as it provides special coverage for their children’s unique needs. Having your child on a health insurance plan means they will experience healthy growth where all their needs are met.

CHIP includes coverage for:

Well-baby doctors’ visits.

Shots and vaccinations.

Hospital visits.

Prescription drug coverage.

Emergency care.

Dental and vision coverage.

Many UnitedHealthcare plans won’t require you to pay for CHIP, while others may need you to pay a small amount each month.

People who fall below a certain pay range may not have to pay for CHIP if they get it through the government. If you earn over a certain amount, you may have to contribute to your CHIP plan.

Dental and vision insurance

UnitedHealthcare covers dental and vision costs, as well as doctors’ visits, medication, and aftercare. Not all of these benefits are standard with all medical insurance plans.

Critical illness insurance

This is a lump sum of cash that is provided to help cover expenses that are associated with a critical illness.

A lump sum is a large amount of money that you receive at once.

Critical illnesses are sicknesses that can kill you or where you may need support from machines to stay alive.

Critical illness insurance covers illnesses like heart attacks, life-threatening cancer, and even a major organ transplant.

Accident insurance

Accidents happen, and the costs of medical care for emergencies can quickly add up.

UnitedHealthcare provides accident insurance to its members in most states. This insurance is paid directly to you to cover the costs of your accident.

Accident insurance pays you cash when you have an accident. This could be anything from a car wreck to a bad fall.

You can choose where you want to get medical care, and you won’t have to choose from UnitedHealthcare’s network of emergency services.

Medicare and Medicare Advantage Plans

Medicare is health insurance for anyone over 65 that the U.S. government provides. You can get Medicare through an insurance company if you want extra benefits.

You can get Medicare Advantage if you need more coverage than the Original federal Medicare.

UnitedHealthcare offers:

Medicate Advantage Plans (Part C): These are plans that pay for medical expenses outside of what Medicare covers.

Medicare Supplement Plans: These are plans for people on Medicare through the government who need extra cover for specific things like hearing and vision.

Medicare Prescription Drug Plans (Part D): These plans are for people who need prescription drugs from pharmacies.

Dual Eligible Special Needs Plans (D-SNP): These are plans for people with disabilities or special needs.

Medicaid Plans

UnitedHealthcare has Medicaid plans. These plans are for people with a low income who need health insurance.

Medicaid covers children, pregnant women, elderly adults, and people with disabilities.

Family and individual health insurance

UnitedHealthcare offers both individual and family health insurance options. Their plans offer lots of extra benefits for your family if you choose one of these.

We will be breaking down these benefits later in this article, but some of their extra benefits are:

Over-the-counter benefits.

In-home visits.

Telehealth visits.

Short-term health insurance

UnitedHealthcare also offers short-term health insurance plans. These plans are for when you only need health insurance for a specific period, rather than needing it all year round.

Short-term insurance is a good idea if you:

Are waiting for your government Medicare to start.

Are between jobs.

Have missed an open enrollment period.

Are turning 26 and coming off your parent’s health insurance.

Premiums and Benefits

Every health insurance provider’s plans include deductibles, co-payments, and out-of-pocket expenses.

You would need to understand each of these because they make up the final cost of your health insurance. Let’s take a deeper look at each of these.

Deductibles

This is the total amount you pay per year that would come from your own pocket for medical care before your plan starts to pay out. You don’t pay this amount annually, you would pay it as you receive medical care.

This excludes preventative services like screening appointments, which are usually automatically covered.

Deductibles depend on the plan you’re on and can affect the total amount you pay for health care costs.

A high deductible health plan (HDHP) may mean you spend less on your monthly premium, but you’re responsible for 100% of out-of-pocket costs until your deductible is met.

A low deductible health plan (LDHP) requires a higher monthly premium but helps you save on out-of-pocket costs.

UnitedHealthcare has a wide network of physicians and other health care providers, making them cheaper than their competitors in terms of deductibles.

Their Balance Bronze plan has a yearly deductible of $7,500 per individual and $15,000 per family.

Their Value Silver plan has an annual deductible of $5,900 per individual and $11,800 per family.

Their Value Gold plan has an annual deductible of $2,350 per individual and $4,700 per family.

Co-payments

These are the payments you would need to make when your health insurance plan does not cover your health care visit in full.

Co-payments usually apply when you receive a health care service.

Your specific plan will determine the price of your co-payment and if you need to make the payment before or after you pay your deductible.

Co-pay amounts are different depending on the plan you choose.

UnitedHealthcare will let you know ahead of time what your co-payments will be so that you can budget for them.

Coinsurance

Until you reach your deductible on a health insurance plan, you are responsible for 100% of your out-of-pocket costs. After you meet your deductible,

UnitedHealthcare will pay a share of your medical costs.

Out-of-pocket costs are money that you will need to pay out of your own pocket for a health service.

Coinsurance is the percentage of the cost of the covered service that UnitedHealthcare will pay for.

For example, if your coinsurance percentage is 20% if you visit a doctor and it costs you $100, your coinsurance payment would be $20 out of your own pocket, while your insurance will cover $80.

Coinsurance differs from one insurance provider to the next and from one plan to the next. But, UnitedHealthcare’s website says that with their plans, you probably won’t pay coinsurance.

Their plans are broken up into three tiers:

Bronze Saver plan has a 30% coinsurance after your deductible.

Silver plan has a 35% coinsurance after your deductible.

Gold plan has no coinsurance, but there is a co-payment.

Premium

Your monthly or annual premium is the amount that you pay, from your own money, to a health insurance provider for health care coverage.

Your premium will depend on the plan you choose and the extra benefits each plan offers.

To find out exactly what your premiums would be with UnitedHealthcare, use their online plan finder tool:

source: uhc

UnitedHealthcare offers a few $0 premium plans, which can be a big plus if you’re looking to save money on health care in retirement.

When we look at the same plans mentioned above, here are what your premiums may look like:

Bronze plan’s monthly premium is $367.99.

Bronze Saver plan’s monthly premium is $380.13.

Gold plan’s monthly premium is $658.33.

Out-of-pocket limit

An out-of-pocket maximum or limit is the highest amount of money you could pay out of your own pocket in one year.

In other words, there is a limit to how much of your own money you will be spending on health care.

With UnitedHealthcare, your deductibles, co-payments, and coinsurance all count toward your out-of-pocket maximum.

Remember -

Deductibles are the amounts you pay for health care services before your health insurance plan starts to pay. If you have a $2,000 deductible, you will pay the first $2,000 of covered services yourself.

Co-payments are a fixed amount that your health insurance expects you to pay from your own pocket to cover your medical costs.

Coinsurance is when you pay a fixed percentage of your health care costs once you’ve paid your deductible. If a doctor’s visit is $100 and your coinsurance is 20%, you will need to pay $20 out of your own pocket when you visit your doctor.

There are two things that don’t get added up toward your out-of-pocket limit: your monthly premium and anything you spend on health care services that aren’t covered by your health insurance.

If you reach your out-of-pocket maximum, your UnitedHealthcare plan will usually then pay 100% of your health care costs, up to a certain amount.

This amount will depend on the plan you choose.

If you reach your out-of-pocket limit, your health insurance will only cover health care that is within their network, and the extra benefits of your plan cover that.

This means that they will only pay for the doctors and visits that your plan covers.

Their Value Bronze saver plan has a $7,000 annual out-of-pocket cost per individual.

Their Value Silver plan has an $8,500 annual out-of-pocket cost per individual.

Their Value Gold plan has an $8,500 annual out-of-pocket cost per individual.

Free screenings

There are certain health care services, also known as preventative care, that are free no matter which health insurance plan you are on.

Preventative care, or free screenings, include:

Routine wellness exams: This is when a doctor checks your general health.

Immunizations: These are injections that stop you from getting sick. Usually, children need immunizations.

Newborn and young infant exams: These covered services are for new babies.

Common tests and screenings depend on your age and gender, but they come at no cost to you.

Benefits you can expect from UnitedHealthcare Insurance

Most Medicare Advantage Plans include extra benefits like:

Dental coverage.

Vision coverage.

Hearing benefits.

This health insurance company also has a program that offers free gym memberships and an online brain health program through AARP's Staying Sharp.

Over-the-counter benefits

Over-the-counter medications are those that a doctor does not prescribe to you. In other words, you don’t need to see a doctor to take these drugs.

You can simply visit a pharmacy and ask the pharmacist to give them to you. These can include vitamins and other supplements, and mild pain medications.

UnitedHealthcare offers a program called FirstLine, which is meant to help its members with a certain amount of money for over-the-counter products.

This means its FirstLine program helps you to pay for your over-the-counter drugs.

In-home visits

When you are unwell or disabled, it can be difficult to get to a doctor for an annual checkup.

UnitedHealthcare provides free yearly in-home visits with a doctor, nurse, or medical assistant.

These medical professionals will perform a physical exam and health screenings at your home without you having to go anywhere.

The information that the doctor gets from an in-home visit will be shared with your primary care provider (PCP).

Terms you need to know -

A primary care provider (PCP) is the doctor you see most often for your general medical care. Seeing the same doctor over timekeeps you healthy and lowers your medical costs.

Virtual visits

UnitedHealthcare offers members telehealth-covered services on their health insurance plans.

Telehealth is when you have a visit with a health care provider without having to leave your home.

You would use technology like a computer, tablet, or phone to speak to your doctor on a video call.

Not all UnitedHealthcare plans cover telehealth visits. The Medicare Advantage Plans do include cover for these appointments.

source: unsplash

Access to a wider provider network

UnitedHealthcare gives its members access to the widest range of medical providers compared to any other insurance company.

As a policyholder, you’ll get access to over 1.2 million doctors and health care professionals, over 6,000 hospitals, and 67,000 pharmacies.

UnitedHealthcare Insurance Ratings

It’s a good idea to look at an insurance provider’s ratings. This will help you decide if they are a good choice for you.

If an insurance company has low ratings, you might want to choose another option.

Consumer Affairs rating

Consumer Affairs is a website that gives companies star ratings based on their customer service. These ratings come from reviews that members write on the website.

UnitedHealthcare’s Consumer Affairs rating is just under four out of five stars, based on over 3,000 reviews.

Their rating of just under four stars is good because many insurance companies only have three-star ratings.

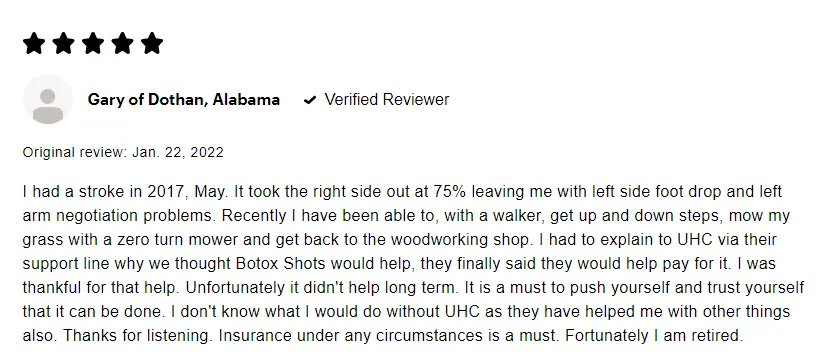

Here is an example of a review left by a UnitedHealthcare member on Consumer Affairs:

source: consumeraffairs

National Committee for Quality Assurance (NCQA)

The National Committee for Quality Assurance (NCQA) is a nonprofit organization that aims to improve the quality of health care that Americans get.

It has certain standards and measures that it uses to decide how good an insurance company is.

UnitedHealthcare’s insurance plans do well when it comes to the NCQA. Many of their plans are high-performing.

Even the plans with the lowest scores are categorized as moderate-performing.

AM Best rating

AM Best is a credit rating agency that looks at how well a company performs financially.

You want to choose a health insurance provider that has good finances so that they can afford to pay for their members’ claims.

AM Best has given UnitedHealthcare an A+ Superior rating. This means that AM Best believes that UnitedHealthcare is a very good insurance company when it comes to its finances.

Comparing Alternatives to UnitedHealthcare

If you are thinking about signing up for a UnitedHealthcare insurance plan, it’s always good to compare them to other insurance providers before you make your decision.

UnitedHealthcare vs. Cigna

Both UnitedHealthcare and Cigna have a lot of health insurance plans for individuals and families, as well as Medicare and Medicare Advantage Plans.

UnitedHealthcare offers health insurance plans in all American states.

Cigna only offers health insurance in 10 states, including Arizona, Colorado, Florida, Illinois, Missouri, North Carolina, Tennessee, Utah, and Virginia.

UnitedHealthcare has 6.5 million members, and Cigna has 15.9 members nationwide.

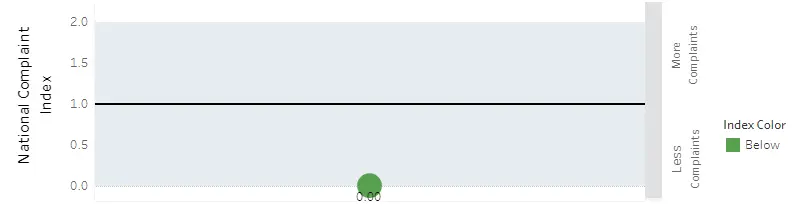

The National Association of Insurance Commissioners (NAIC) is an organization that regulates health insurance in the U.S.

NAIC has a Complaint Index which is the number of complaints they receive from a health insurer’s members.

The starting point of the national Complaint Index is always 1.0—this is neutral and can move in either direction based on if there are more positive reviews or more complaints.

If a company has a Complaint Index of 2.0, they get many complaints. If they have a Complaint Index of 0.5, they get fewer complaints and more positive reviews.

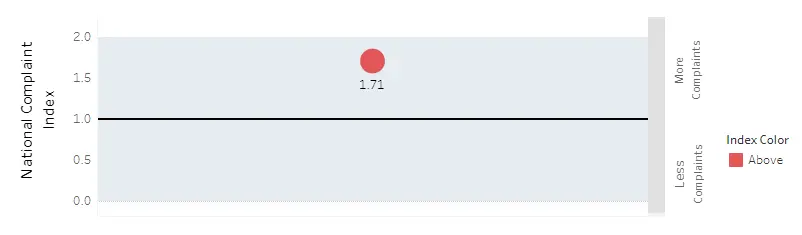

UnitedHealthcare has an NAIC Complaint Index of zero. Cigna has an NAIC Complaint index of 1.71..

Here is UnitedHealthcare’s NAIC Complaint Index:

source: NAIC

Here is Cigma’s NAIC Complaint Index:

source: NAIC

UnitedHealthcare vs. Humana

Compared to UnitedHealthcare, Humana health insurance has fewer plans available. But, Humana’s plans are cheaper than UnitedHealthcare.

Humana doesn’t offer individual or family medical, and hospital coverage like UnitedHealthcare does.

Like UnitedHealthcare, Humana has health insurance plans available in every state.

Both companies have a mobile app, and you can access and manage your account online or via phone.

Here is what the UnitedHealthcare app looks like:

source: uhc UnitedHealthcare has over 1.3 million doctors and 6,500 hospitals that they cover. Humana only has 22,000 covered doctors.

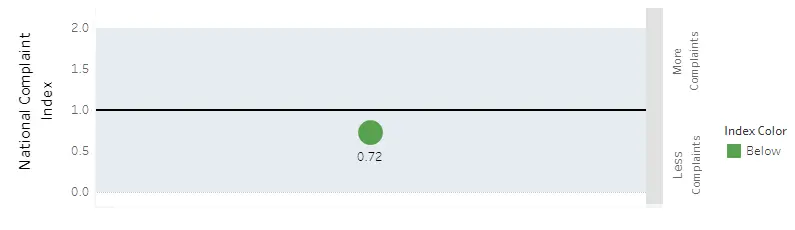

Humana has an NAIC Complaint Index of 0.72, which is very high compared to that of UnitedHealthcare.

Here is Humana’s NAIC Complaint Index:

source: NAIC

UnitedHealthcare vs. Blue Cross Blue Shield

Blue Cross Blue Shield (BCBS) was the first ever health insurance plan in the country. Its plans are available in all 50 states, and they have over 62 million members.

BCBS covers over 342,000 doctors and health care providers across the U.S. It offers customer service options, including:

Online account management: You can log into your health insurance account online and manage and monitor your plan.

A dedicated customer care line: You can call BCBS via telephone if you need help with anything related to your health insurance.

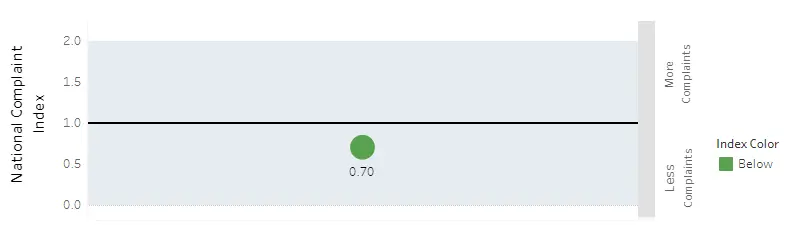

They have an NAIC Complaint Index of 0.70, which isn’t bad considering it should be 1.0 or lower.

Here is Blue Cross Blue Shield’s NAIC Complaint Index:

source: NAIC

Our Final Verdict on UnitedHealthcare

Because they are the largest health insurance provider in the U.S., UnitedHealthcare is a good option because they offer the most plans to choose from.

Their plans are more expensive than some other companies, but their extra benefits are very comprehensive, and they cover a large number of doctors and health care providers.

They have good ratings across the board, which shows that their members are happy with them.

We aim always to provide you with the best information about each health insurance company so you can make the right decision.

If you need more help, you can call us at 1-888-912-2132 or send an email to Help@PolicyScout.com. Our trained consultants are ready to help you.

Frequently Asked Questions (FAQs) about UnitedHealthcare

Is UnitedHealthcare a good network?

UnitedHealthcare has a large provider network and offers a range of extra benefits for members.

They have the widest range of plans for you to choose from, which means you can find the right option for you.

They have very positive ratings from their members and other organizations, which means they deal with customer issues very well.

What’s the difference between AARP and UnitedHealthcare?

The American Association of Retired Persons (AARP) is an interest group in the U.S. that focuses on issues that affect people over the age of 50.

It is not an insurance company, but it offers health care insurance plans through UnitedHealthcare.

AARP Medicare Advantage Plans through UnitedHealthcare offer lots of extra benefits, and they help cover out-of-pocket costs.

Is UnitedHealthcare a good plan for seniors?

UnitedHealthcare’s Medicare Advantage Plans for seniors offer good coverage for medical expenses.

They even have plans for as little as $15 per month for senior people. They also have good supplemental insurance, as well as dental and vision plan options.

Their free benefits for in-home doctors’visits and telehealth options are great advantages for elderly people who may not be able to visit a doctor’s office.

How can I learn more about United Health Medicare Advantage and Medicare Prescription Drug Plans (PDPs)?

To reach UnitedHealthcare, you can:

Call them at 800-607-2877 on any day between 7 a.m. and 10 p.m.

Make an appointment to see one of their agents by phoning the same number.

Visit their website to find more information about a plan for you.

Current members can contact UnitedHealthcare by calling the phone number on the back of their member ID card.