The High Cost of US Healthcare

Healthcare costs in the United States are among the highest in the world, but does that make us any healthier? PolicyScout takes a deep dive into what costs we face, what are the issues, and what does it mean for the current coronavirus pandemic.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

Healthcare costs in the United States have reached critical mass. According to the CMS, Centers for Medicare and Medicaid Services, the 2018 costs for healthcare goods and services, health insurance, public health activities, government administration, etc., reached 3.6 trillion dollars, which translates to $11,172 per person. Those figures reflect a 4.6 percent increase in costs and means health care is 17.7 percent of the US's Gross Domestic Product.

If those figures sound frightening, they should. The US healthcare system has weaknesses that have been exacerbated in recent years, inspiring experts to call for action. With the COVID-19 pandemic roiling US society, conditions are only getting worse. In this election year, the policy debates are growing more heated about how to fix the system. People don't agree on how to fix the problem, but they do agree that a fix is essential.

The State of US Health Care

The US spends more on health care, based on its share of the economy, than the average OECD, or Organization for Economic Co-operation and Development, country - twice as much in fact. Sadly, this high level of spending is not delivering positive results, especially when compared to ten other high- income countries: Australia, Canada, France, Germany, the Netherlands, New Zealand, Norway, Sweden, Switzerland, and the United Kingdom. The United States has the following healthcare negatives:

The lowest life expectancy of the 11 nations.

The highest suicide rate of the other countries.

The highest level of chronic disease and twice the rate of the OECD average.

Fewer physician visits than those in most countries.

The highest number of hospitalizations from preventable causes when compared to peer nations.

The highest rate of avoidable deaths.

The findings were not all bad. The US leads its peer nations in preventative medicine, including breast cancer screenings and vaccinations. It also more frequently uses advanced technology for certain procedures and testing, such as MRIs, although some experts argue that providers overuse this technology.

Healthcare Insurance Coverage

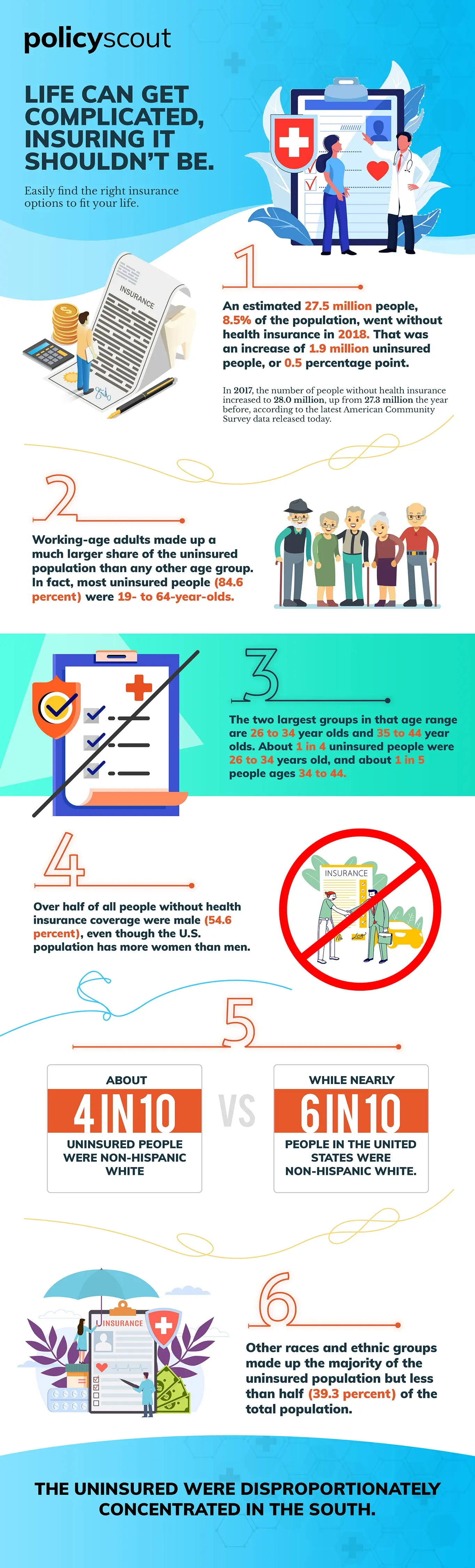

Despite the United States' standing as a leader among industrial nations, its health insurance system is considered uneven at best. According to 2018 figures, 8.5 percent of the population, or 27.5 million people, were uninsured, an increase of 1.9 million from 2017.

Most of the uninsured were working-age adults, and in that large group, 1 in 4 was 26-34 years old. The majority of uninsured were male, although women make up over half of the population.

Also, race is a factor in insurance coverage. Although 6 in 10 citizens were non-Hispanic white during this period, only 4 in 6 of the uninsured population were non-Hispanic white. In fact, the minority populations made up the largest percentage of the uninsured although they only accounted for 39.3 percent of the US population.

Other facts about uninsured demographics include:

They are disproportionately clustered in the South.

14 per cent of the uninsured are age 19 or younger.

Just 1.4 percent of those 65 or older are uninsured, due, no doubt, to Medicare coverage.

Based on the data gathered from the American Community Survey conducted by the Census Bureau, the uninsured tend to be 19 to 64 years old, are male, and do not have a high school diploma. The uninsured also tend to earn an income on the lower end of the scale.

Healthcare Procedure Costs

Many factors influence the cost of healthcare in the US, leading to shocking price tags on basic procedures and services. For instance, US citizens pay about four times what the citizens of other industrialized nations pay, largely because the government does not regulate drug prices the way many European countries do. It's not uncommon for US citizens to go without important medications because they cannot afford them. Recently, some diabetics have harmed their health by skimping on insulin due to the high cost of the medication. A number of deaths have also resulted from this medication rationing.

The cost of an ambulance ride often adds up to $2500, which famously shocked British citizens whose National Health Service completely covers their ambulance service. The cost of generic Epipens is $400 per two-pack. in the US, while In Canada, this medication is approximately half of that price. People do die in the US because they cannot afford the care they need.

Prices for common medical procedures in the US include the following:

Knee replacement - $35,000

Hip replacement - $40,364

Angioplasty - $28,200

Gastric Sleeve - $16,000

Heart Bypass - $123,00

Daily Hospital cost - $3,949

Of course, prices for procedures vary according to the provider. An MRI, for instance, can cost between $400 and $3500, depending on the exact type of MRI performed, what body part is involved, and the individual provider. United States healthcare system prices are simply inconsistent. The costs and variations in pricing are quite stunning to those living in countries with more government-controlled health care.

Healthcare Insurance Costs

United States medical costs are spiraling upward, and while there is no one solution to the problem, better health insurance can help. A solid insurance policy mitigates many of these costs and allows US citizens to get much of the care they need. Even with insurance, however, the price tag for medical services is high, partly because of the skyrocketing cost of the insurance itself.

Since 1984, the yearly cost of insurance has risen 740%, meaning the average person now pays around $3400 each year for coverage. Many people find paying for their monthly premiums is difficult. And if they actually seek medical attention, their coverage will require that they pay for deductibles, coinsurance, copays and uncovered expenses. Excellent insurance certainly helps people pay for medical services, but patients will still incur significant costs.

Employer-based Insurance

In the United States, many people get their coverage through their employers, a practice that began after WWII. Providing health insurance was a way to increase employee benefits, provide tax benefits for employers and employees and fight against inflation. Currently, more than 50% of Americans under 65 get their health insurance through an employer, a total of 158 million people. About 25% of Americans purchase individual plans, many through the Healthcare Marketplace. Although the number of employer-based plans is still high, they have decreased in the last few decades. Healthcare analysts question continuing this relationship between employment and insurance, a tie that does not exist or is not as strong in other countries.

Average Health Insurance Premium Costs

The costs of health insurance policies varies widely in the US, depending on a number of factors, including geographical location, state law and the level of coverage. In 2019, the average cost of insurance for a family of four was $20,576, although employers covered approximately 71 per cent of that amount. For those buying coverage on the Healthcare Marketplace, the cost often depends on personal income since the Affordable Care Act subsidies can reduce premiums by thousands of dollars each year.

The cost range is perplexing when experts compare premium prices for 27-year-old people in the US. The same policy that costs $295 per month in Michigan costs $723 in Wyoming. These wide swings in premiums often confuse and frustrate American consumers and seed distrust in the system.

Out-of-Pocket Expenses

Insurance policies are not pay once and be completely covered. The premium is only the beginning of insurance costs. Consumers are required to pay much more for out-of-pocket expenses, which depend on the level of coverage their policy provides. In 2018, the average out-of-pocket expense per person was $1242. These out-of-pocket costs include the following:

Deductible - A policy's deductible is the amount that must be met before the policy pays for covered services. This amount may be as low as several hundred dollars or as high as $5000 or more. Higher-deductible policies cost less because they don't have to pay out as often. High-deductible policies are often used as catastrophic coverage - meant to protect the buyer in case of major surgery or other big medical expense. They aren't expected to help much with the smaller bills.

Co-pays - Co-pays are the "upfront" fees you pay before seeing your physician. The copay amount varies according to your policy's level of coverage and whether the provider is a GP or specialist. The amounts are generally quite low - sometimes $20 or so. Copays are generally separate from the deductible, meaning you don't have to meet the deductible before the copayment provisions kick in. In some policies, your copays do count toward meeting your deductible, however.

Co-insurance - Insurance policies do not pay all of your medical claims, at least not until you reach your out-of-pocket maximum. Once you reach that maximum, your policy should pay 100% of your valid claims. Until then, you will be responsible for a percentage of the costs, often 20% or more.

Drug Co-pays - Your pharmacy costs also vary according to your specific policy. You will usually pay a different amount for generic drugs versus name brand offerings. Plus, your insurance company prepares a formulary or list of drugs that a panel of experts determines are most effective. These drugs are then placed into 4 tiers. As the tier number rises, so do your costs. And drug companies do not agree on what drugs should be preferred or non-preferred choices, so the drug you could afford last year may be out of reach this one if your policy changes.

Americans tend to pay much more in prescription costs than other industrialized nations, in part due to lack of competition between drug companies and the limited US government control over what is known as "big pharma."

Consumers have difficulty predicting what their total insurance and healthcare costs will be simply because insurance plans vary so much as does their health status. Obtaining the right, affordable protection is always a challenge, even with an employer-sponsored plan.

Coronavirus Costs

The COVID-19 pandemic has thrown more uncertainty into US healthcare. Now the epicenter of the crisis, the US has struggled to administer necessary testing. The cost of testing has been a challenge for some, although the cost of treatment has been the biggest worry. Severely ill COVID-19 patients may be hospitalized for weeks and require round-the-clock care. The price tag for this care can be astronomical.

Testing

Congress mandated that COVID-19 tests would be free for all Americans. However, many people have been surprised by medical bills associated with these tests. The actual test may be free, but providers may charge for the pre-screening. They will definitely charge for any additional tests they deem necessary. Also, insurance companies may have to cover certain costs upfront and work to be reimbursed by the government after the fact. Many patients have received hefty testing bills that they were not expecting.

Covid-19 Care

For some patients, recovering from COVID-19 means staying at home and taking OTC medications or treatments. The biggest issue is the loss of work, which should be covered under DOL regulations. The big costs come from hospitalization and long-term medical issues.

Experts estimate that 15 to 20% of COVID-19 patients need to be hospitalized for this condition. A recent study by Fair Health analyzed the costs associated with these patients and found that the average charge per uninsured patient was $73,300. An insured patient could expect a $38,221 bill. However, that amount includes what their insurance plan would pay plus what their contribution would be. The actual cost to the patient depended on their deductible, co-insurance, and out-of-pocket maximum. In any instance, the price for contracting COVID-19 is an expensive one in terms of medical bills, loss of work and potential long-term effects.

Recently, researchers have been studying the health of so-called "long-haulers," those COVID-19 patients who suffer from symptoms months after they test negative for the virus. Many survivors complain of headaches, fatigue, dizziness, cardiac problems, breathing issues, etc. Scientists suspect that the virus, even in asymptomatic people, may cause permanent damage on the cellular level. Since millions have tested positive for the coronavirus in the US, these long-haul ailments will put pressure on an already over-taxed healthcare and health insurance network. The ultimate societal and cultural effects of COVID-19 will be overwhelming. The actual financial cost simply cannot be calculated at this point.

Final Thoughts

Healthcare costs in the United States are not sustainable, especially in the face of a global pandemic. And while other countries are also facing increased pressure on their healthcare systems, their citizens are paying much less for care. In the US, citizens are still largely reliant on their employers for health insurance, and these employers are having trouble providing this coverage due to increased costs. In fact, some economists attribute stagnating wages to the cost of employers for employee healthcare. And while the number of uninsured Americans dipped after the passage of the Affordable Care Act, that number is again rising, in part due to legal challenges to provisions of the law.

Healthcare reform is a huge issue in this year's presidential election on all sides of the political spectrum. No matter who wins in November, these costs will have to be addressed or more Americans will go without the medical care they need or see themselves mired in horrifying debt.

PolicyScout

If you are shopping for an insurance policy, you need help to find the most affordable option with the benefits you require. PolicyScout lets you comparison shop hundreds of policies in just minutes, making your selection process so much easier. You only need to enter your zip code to get started.

In this time of so much uncertainty, you need a healthcare policy that you can count on. Going without insurance is really not an option. Use PolicyScout today and find the coverage you need to protect you and your family from catastrophic medical bills.