What Age Does Car Insurance Costs Go Down?

Find out how your age will affect your car insurance rates and when your premiums will go down.

Our content follows strict guidelines for editorial accuracy and integrity. Learn about our and how we make money.

If you’re a young driver in your teens or early twenties, you’ll generally pay more for auto insurance cover. This is because younger drivers have a higher risk profile than older drivers according to insurance providers.

The Insurance Information Institute estimates that drivers between the ages of 16-24 have a higher likelihood of being involved in a fatal accident than any other age group.

Read our guide to learn when your car insurance rates will decrease, and find out what you can do to get a better deal while you wait.

How Auto Insurance Rates Are Set

Car insurance rates are set by insurance companies and are based on a number of factors, including the period of coverage, the amount of coverage, and the risk profile of the driver.

Insurance companies use underwriting to assess the risk of insuring a particular driver, and rates are generally higher for drivers who are considered to be a higher risk.

What Is Underwriting?

Underwriting is the process of evaluating a potential customer's risk profile and then setting rates and coverage terms accordingly.

This evaluation generally takes into account factors such as the individual's age, health, occupation, and criminal record.

Once the underwriter has determined the amount of risk involved, they will set rates that reflect that risk. For example, someone with a clean driving record and no health problems will generally pay lower rates than someone with a history of accidents or a chronic health condition.

Let’s cover a few of the factors that insurance companies use to determine insurance rates.

1. Age

Age will play the largest part in determining your risk and car insurance rates. Younger drivers pay more for insurance because statistically, they are more likely to be involved in an accident than someone older.

2. Gender

Gender is another large factor that car insurance companies use to calculate insurance rates. According to national statistics, men are more likely to be involved in traffic accidents than women.

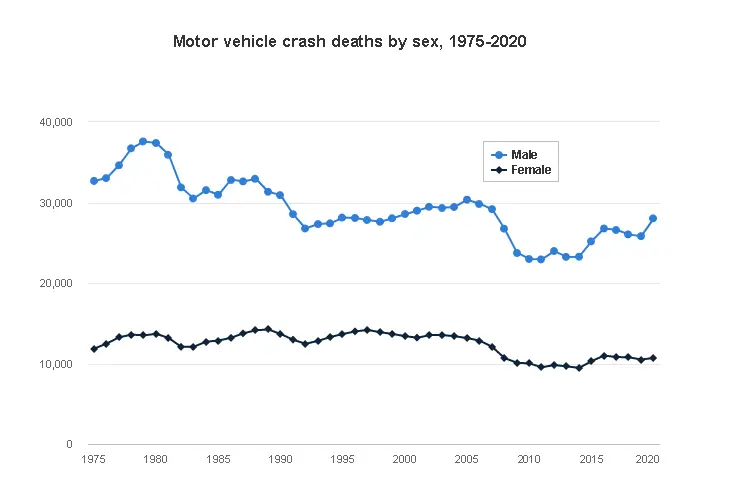

This graph produced by Insurance Institute for Highway Safety (IIHS) shows the difference in motor vehicle accident deaths based on gender between 1975 to 2020.

However, this is a contentious topic as this business practice excludes nonbinary and trans people. In some states, it is against the law to factor gender into rate calculations for auto insurance.

3. Driving record

Your driving record plays a big role in the price you’ll pay for your insurance. If you have a clean driving record, then you’ll pay less for coverage than someone with speeding tickets, accidents, and DUIs.

4. Where you live

Insurance companies also look at your location when determining the cost of insurance. They look at factors such as the number of accidents that happen in your county and the average income level in your area.

If you live in an area with a high accident rate, you’ll generally have to pay more to be covered. This is because the statistical chances of an accident happening are higher.

Similarly, if you live in an area where the average income is high, you’ll need to pay more insurance. This is because your insurance company will potentially have to cover higher repair costs if you’re involved in an accident.

5. Your car

Your cost of coverage will depend on the value of your vehicle and its condition. If you drive a new luxury car, your insurance will be higher than if you drive a secondhand sedan.

Another factor to consider in this category is how easily parts can be sourced for your vehicle and what they cost. For example, if you drive a vehicle that has expensive parts that are hard to get, you’ll likely pay a higher monthly rate for your auto insurance.

6. Your insurance provider

If you’ve ever used an online quote finder, you’d probably have seen a range of prices from different auto insurance companies.

Auto insurance rates will vary from company to company based on their size, focus, risk profile, their methods of calculation, and other factors.

For example, a larger insurance company may be able to offer you a lower rate because they have large cash reserves. Another smaller insurance company may again be able to compete on price because they focus on drivers like you.

7. Your credit record

You may be thinking, what does my credit record have to do with my car insurance? Well, insurance companies are in the business of managing their risk. They look at the risk profile of each person that applies to figure out how risky their business with them will be and whether they should insure them.

Top Tip: Find Out How Your Insurance Company Will Calculate Your Risk Profile

Your insurance company uses a number of factors to calculate your rates and determine your risk profile.

They will consider the type of coverage you need, the period of time you need it for, and your personal information. This includes your age, gender, marital status, job, and driving record.

Insurance companies use this information to assess your likelihood of making a claim. The more risk you pose, the higher your rates will be.

If you’re working with an insurance agent, you should ask them how your preferred provider calculates their risk profiles. You can also find out whether your credit record will impact your costs.

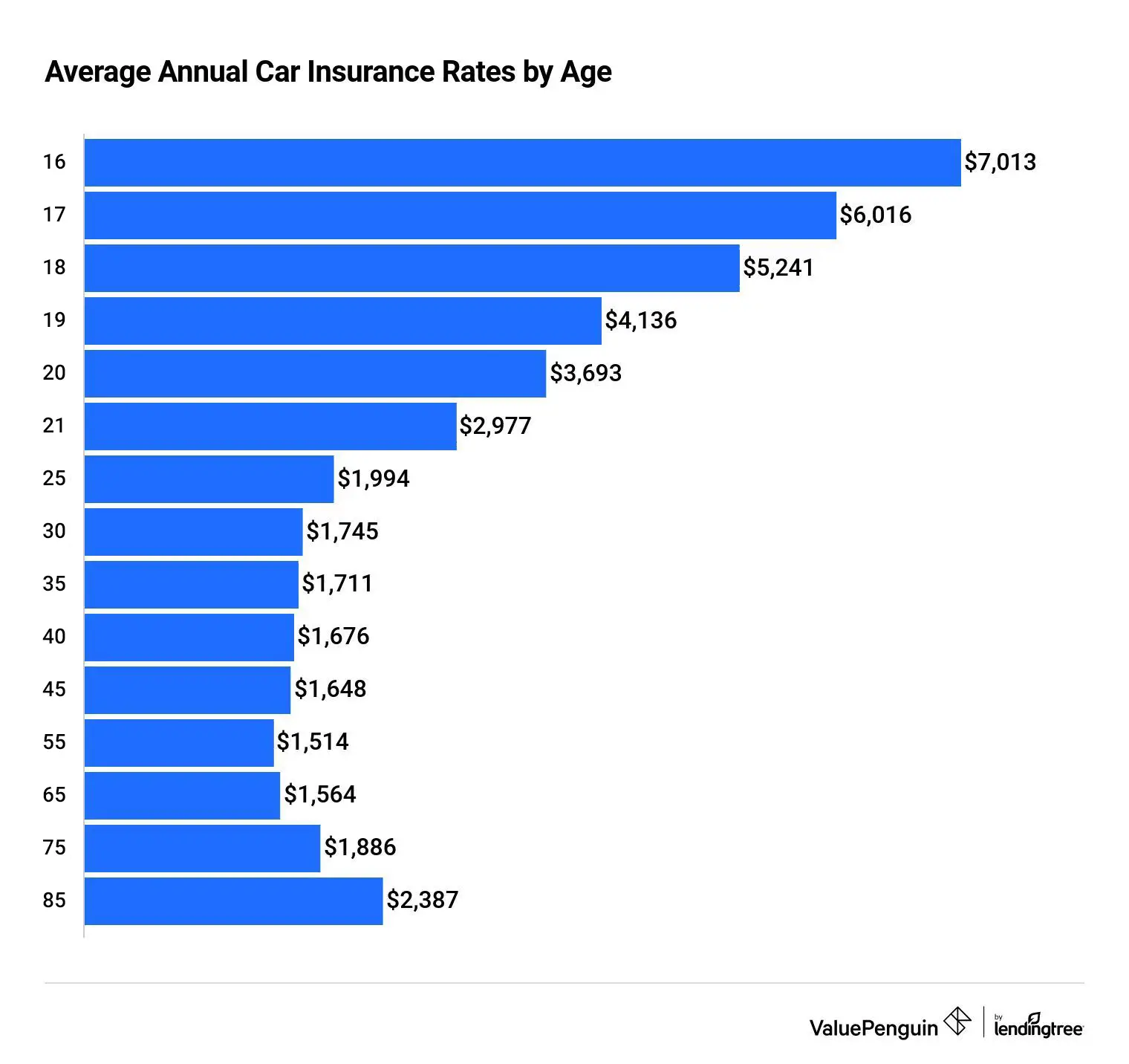

At What Age Does Car Insurance Go Down?

Your car insurance rates will generally go down when you turn 25. This is because risk factors go down as drivers gain more experience and get older. Some of these risk factors include:

Inexperience with driving.

Nighttime and weekend driving.

Not using seat belts.

Distracted driving.

Speeding.

Alcohol use.

Insurance rates tend to decrease from age 25 and above. However, there are a number of factors that can affect potential savings.

For example, the type of coverage and the length of the policy period can both play a role in determining your auto insurance premium. In addition, some insurers may offer discounts for drivers who have clean driving records.

Keep in mind that as you get older, your car insurance rates will decrease. However, once you reach the age of 65, car insurance rates go up again.

Source: ValuePenguin

What Younger Drivers Can Do to Lower Their Car Insurance Rates

Car insurance rates for young drivers can be quite high, but there are some things that can be done to lower them. The best option for young drivers is to shop around and compare rates from different companies.

By taking some time to research their options, young drivers can find ways to save on their car insurance rates. Here are some steps you can take to lower your car insurance rates:

You’ve avoided traffic accidents

If you’re a young driver and don’t have accidents on your record, your insurance rates will decrease faster. Keep in mind that you’ll still be paying higher rates for coverage until you turn 25.

You move to another insurance provider

If you shop around for your car insurance, you might be able to find a better rate for the same amount of coverage. There are companies that specialize in insuring specific types of people, including young drivers.

Use our insurance quote finder to see if you can get a better deal or reach out to one of our agents to speak about your options.

You’ve done driving courses or certifications

One way to lower your monthly car insurance premium is to do defensive driving courses that are recognized by your state. Your car insurance provider will likely offer you a lower car insurance rate if you’ve completed courses that will improve your driving skills.

How Much Is Car Insurance for a 25-Year-Old?

It is difficult to say how much car insurance will cost for a 25-year-old without knowing more about their specific circumstances.

Rates for car insurance vary depending on a number of factors, including the driver's age, the type of vehicle being insured, the length of the policy period, and the amount of coverage.

However, rates can also be affected by the driver's risk profile, which is determined by factors such as their driving history, credit score, and claims history.

For a 25-year-old driver, rates will typically be higher than they are for older drivers, but they will still be affected by the driver's individual risk profile.

If you’d like to find out what you’ll pay for car coverage, use our online quote finder, or reach out to us on 1-888-912-2132 or help@policyscout.com.

How Long After a Ticket Does Your Car Insurance Go Down?

Getting a speeding ticket or other traffic violation notice can cause your car insurance premiums to jump up. But, this doesn’t mean you’ll be stuck with higher rates forever.

Tips to Lower Your Car Insurance after an Accident

Rates usually go up after an accident, but there are a few things you can do to help offset the increase.

Shop around for a new car insurance policy. Rates can vary widely from company to company, so it's worth it to take the time to compare rates.

Consider raising your deductible. This will lower your rates, but it's important to make sure that you can still afford the deductible if you do have an accident.

Make sure that you're getting all the discounts you're entitled to. Many auto insurance companies offer discounts for things like a good driving record and installing safety devices in your car.

Tips for Switching Car Insurance Companies

As we’ve mentioned above, switching car insurance is a good way of finding lower rates. If you’re thinking about changing your car insurance provider, here are some tips to help you find the best deal around.

Use an auto insurance agent: If you don’t want to spend the time researching insurance types, providers, and costs, use an car insurance agent to do it for you. You won’t have to pay anything for their services.

Compare benefits along with costs: Some people only look at costs when deciding on car insurance. Our advice is to look at what you’re getting in return for your car insurance premiums every month. Does your car insurance provider offer free roadside assistance? Do they have a high customer satisfaction rating? Do they cover windshield damage?

Get the best coverage you can afford: Insurance is meant to protect you and your property against damage, theft, and vandalism. Getting more coverage than your state’s minimum liability might cost you more each month, but it’s worth it if you’re involved in a serious accident.

Do your own research: If you’re not sure which provider to use, go online and find out what other people think of the company, look at their financial ratings, and ask your friends and family what they think before you sign any contract.

Look for companies that specialize in filing SR-22 bonds: If you need SR-22 insurance, these companies will typically offer more competitive rates than other insurance companies.

See if you can bundle your insurance coverage: If you already have home or life insurance through a particular insurance provider, call your agent and ask whether they can bundle your coverage and offer you a better rate.

Where Can I Learn More about Auto Insurance?

Getting auto insurance for young drivers should be a priority. However, expect to pay more for coverage until the age of 25.

There are some steps you can take if you want to get a better deal on your current car cover. Young drivers can shop around, use an insurance agent, and keep their driving record clean to put a dent in insurance costs.

If you’d like to learn more about auto insurance, reach out to one of our expert advisors today to compare plans, find coverage, and see what the best deals are in your area.